FINANCIAL FREEDOM

BUILDING FINANCIAL FREEDOM

Does the idea of planning for your financial future seem too complex or confusing? Do you think you can't save money because you're barely making ends meet as it is? All excuses aside, there are two good reasons to seize

control of your finances now:

You can no longer count on your employer or the government to provide for you now or in the future. You must make your own plans.

Financial planning is the key to paying for those big ticket items — buying your own home or funding a college education for your children.

The sooner you start planning for the future, the sooner you'll reap the rewards. Use this guide to help you build your financial freedom.

Establish a Spending Plan

The first step toward financial freedom is establishing a spending plan. The worksheet below will show you how much money you have coming in and going out. Fill in the monthly dollar amounts for each item below. Then,

subtract your total expenditures from your total income.

This is the amount you can save without making any changes in your spending habits. A recommended savings rate is 10% of your take-home pay. If you find that your total is a negative number or is less than you would like to

save, you need to find areas where you can cut spending. Begin by recording all your expenditures for one month (cash, check and credit) in a notebook so you know exactly where your money is going. Look for areas where you

can cut back. Perhaps you can rent videos rather than going to the movies, cut down on your dry cleaning bill, use coupons at the grocery store, carpool to work or take your lunch rather than eating out.

Once you have determined how much you can save each month, enter this amount on your worksheet as one of your permanent expenditures. Pay yourself first by setting aside your savings when you receive your paycheck,

before you have a chance to spend the money on anything else. It helps to have savings automatically deducted from your paycheck or checking account. Don’t get discouraged if an emergency cuts into your savings. Just get

back on track the following month.

Does the idea of planning for your financial future seem too complex or confusing? Do you think you can't save money because you're barely making ends meet as it is? All excuses aside, there are two good reasons to seize

control of your finances now:

You can no longer count on your employer or the government to provide for you now or in the future. You must make your own plans.

Financial planning is the key to paying for those big ticket items — buying your own home or funding a college education for your children.

The sooner you start planning for the future, the sooner you'll reap the rewards. Use this guide to help you build your financial freedom.

Establish a Spending Plan

The first step toward financial freedom is establishing a spending plan. The worksheet below will show you how much money you have coming in and going out. Fill in the monthly dollar amounts for each item below. Then,

subtract your total expenditures from your total income.

This is the amount you can save without making any changes in your spending habits. A recommended savings rate is 10% of your take-home pay. If you find that your total is a negative number or is less than you would like to

save, you need to find areas where you can cut spending. Begin by recording all your expenditures for one month (cash, check and credit) in a notebook so you know exactly where your money is going. Look for areas where you

can cut back. Perhaps you can rent videos rather than going to the movies, cut down on your dry cleaning bill, use coupons at the grocery store, carpool to work or take your lunch rather than eating out.

Once you have determined how much you can save each month, enter this amount on your worksheet as one of your permanent expenditures. Pay yourself first by setting aside your savings when you receive your paycheck,

before you have a chance to spend the money on anything else. It helps to have savings automatically deducted from your paycheck or checking account. Don’t get discouraged if an emergency cuts into your savings. Just get

back on track the following month.

| Other Ways to Build Your Financial Freedom Social Security. You’ve paid into it most of your life, so don’t forget to include it in your financial planning. The income you receive when you reach the eligibility age (e.g., 65) is based on the average of your 35 highest salary years. You also can collect 80% of your benefit at age 62. If you die, your spouse may be entitled to your benefits. The age at which you can collect full benefits is currently scheduled to increase gradually to 67. You can check the record of your earnings and get a statement of your anticipated benefits by calling Social Security at 800/772-1213. Life Insurance. Life insurance can help to financially protect your loved ones in the event of your death. It’s important if you are married and even more important if you have dependent children. There are several types of life insurance: Term life insurance pays a fixed amount of money to your beneficiary if you die during the term of the policy. The cost of premiums increases as you get older. Whole life insurance is permanent insurance that provides a death benefit that is guaranteed for the insured's life as long as premiums are paid. Participating policies may pay dividends that can increase the policy's cash value, but they are not guaranteed. Universal life insurance is considered a variation of whole life insurance with more flexibility. Within limits, the policy owner determines the amount and frequency of his or her premium payments and is permitted to adjust the policy face amount up or down to reflect changes in his or her needs. As premiums are paid and cash values accumulate, interest is credited to the policy's accumulation fund. Variable Life Insurance is similar to universal life in that there is flexibility in connection with premium payments and death benefits. However, with variable life, premium payments are held in separate accounts, and the policy owner chooses how the cash value will be invested. Consequently, such a policy's cash value will fluctuate with the performance of the chosen investment portfolios. Health Insurance. Health coverage protects you in case of sickness or injury. Without it you run the risk of being financially wiped out by just one serious illness or accident. Most people receive subsidized health benefits through their employer, but coverage can also be purchased as an individual. Disability Insurance. This is probably one of the most overlooked forms of insurance for working-age people. Disability coverage replaces a portion of your income when you can't work because of illness or injury. Most policies replace 60% to 80% of your income. (You also may receive income from Social Security for certain disabilities, or from Workers Compensation if you are injured on the job.) If your employer provides a 60% disability policy, you might want to consider a supplemental policy covering 20% of your income. Long Term Care Insurance. Long Term Care insurance is designed to help pay for nursing home care, assisted living care or home health care expenses. This fast growing type of insurance can protect you and your assets against the high cost of long-term care. Most policies pay benefits when long-term care is prescribed by a physician as medically necessary or when someone can no longer physically or mentally take care of basic needs. Homeowners Insurance. Homeowners coverage protects your financial investment in your home. It provides compensation for damages to your home and its contents, and it may protect you from financial liability if someone is injured on your property. The extent and amount of coverage needed depends on your situation, but if you can afford it, it is wise to insure your home for 100% of its replacement cost. Auto Insurance. Auto insurance is more than a matter of insuring your vehicle for loss or repairs after an accident. It is a financial safety net that can help you offset the cost of bodily injuries to yourself or others, lost wages due to injury, and lawsuits brought against you as the result of an accident. Most states require the purchase of basic coverage and then you determine the additional insurance you need. Estate Planning. Another way to safeguard your family’s financial future is through estate planning. Generally, estate planning includes taking an inventory of your assets and making a will or establishing a trust, with an emphasis on minimizing taxes. Estate planning is very complex and subject to changing laws. You may want to seek professional advice. Do You Need a Financial Advisor? If you need help with your blueprint for the future, you may want to consult a financial advisor, a CPA or even a lawyer who can give you advice on everything from budgeting, taxes, retirement and estate planning to investments, insurance and real estate. Some financial advisors charge you no fee; instead they make a commission on the financial vehicles that they sell you. Other advisors are fee-only, which means they charge you for their services but do not make a commission on financial products you buy. Still others charge a fee for providing the financial plan and may also receive commissions if they sell you any products. Shop around and talk to several financial advisors. Be sure you feel comfortable with them and can understand their explanations. Ask for their credentials. One credential is a Certified Financial Planner (CFP) designation, which means the planner has taken a series of courses in financial planning, has passed an exam, has at least three years experience and takes continuing education courses each year. Other designations include Chartered Financial Consultant (ChFC), Certified Public Accountant (CPA) and Registered Financial Planner (RFP). Investment advisors and broker/dealers may also be regulated by the state. The Securities and Exchange Commission (SEC) regulates broker/dealers and some investment advisors. Individuals associated with these firms generally must pass certain licensing examinations. Brokers vs. Online Services If you plan to buy stocks or bonds as part of your investment portfolio, you will need to either choose a broker (full service or discount) or sign-up for an online service. A broker is a licensed professional who monitors investments and gives advice on stock purchases for a fee. The fee can be either a percentage of your portfolio or a per transaction fee. Brokers may also make commissions on some of the investments they sell. Before selecting a broker, make sure your candidate is part of the Securities Investor Protection Corporation (SIPC), a nonprofit corporation that can protect your interests up to $500,000 if the broker should become insolvent. Also call the National Association of Securities Dealers’ (NASD) toll-free hotline at 1-800/289-9999. The NASD can tell you if there has been any disciplinary action against a particular brokerage firm or sales representative. Discount brokerage houses generally have lower fees than those touted as full-service. They employ brokers who, primarily, are order takers and may, or may not, give investment advice. If you use a discount broker, be sure you are well-informed about stocks and can make your own investment decisions. Online services allow you to buy your own stocks, bonds, and mutual funds for significantly lowered fees, but not without risk. Although research is available, you are making your own investment decisions. Most online services provide varying levels of research, news and customer service. You should also become familiar with the online brokerage commission schedule and fees before joining or trading through an online service. Keep in mind, too, that some online services offer delayed quotes, others have real time quotes; some excel at customer service and, for others, it may be nonexistent. Online services have different levels of strengths so, again, be well-informed before using one. However you decide to buy stocks, from a full service broker, discount broker or online service, research each option carefully and make sure it meets your investment needs. Tips for Investors Shop around. Compare the products and fees of various banks, financial planners, brokers and investment houses. Ask questions. All investments carry some degree of risk, so you should fully understand what you are getting into. Ask for a written explanation of products, operations and fees. Educate yourself. Spend some time at your local library gathering information. Read investment and financial publications such as the Wall Street Journal, Barron's, Investor's Business Daily, Money, Smart Money, Forbes and the monthly Standard & Poor's Stock Reports. Moody's Investors Service also has manuals that contain financial information on thousands of companies. Get advice. A financial advisor, your accountant or tax advisor are all good sources of information to help you understand the choices you are making and what your risks will be. Make sure any salesperson or advisor understands your goals and how much risk you are willing to assume. Don't buy stocks or other investments pitched to you over the telephone. And never let a salesperson pressure you into acting immediately. Be suspicious if a salesperson promises a spectacular rate of return. If it seems too good to be true, it probably is. Don't put all your eggs in one basket. Diversification — distributing your money across different types of investments — is the key to sound investing. Never invest in a product you don't fully understand. Finally, re-evaluate your financial plan regularly. Also, stop and review your plan whenever you marry, divorce, have a child, buy a home or retire. For More Information |

FINANCIAL FREEDOM: A SMARTEST WAY TO PREPARE A BETTER FUTURE IS TO PLAN TODAY TO OBTAIN A COMPLETE FINANCIAL FREEDOM.tomorrow

| BUYING, SELLING, LEASING A PROPERTY IN SOUTH FLORIDA. PLEASE CALL A PROFESSIONAL REALTOR IMPORTANT TOOLS ARE NEEDED TO SUCCEED IN REAL ESTATE INVESTMENTS. The real estate market can be lucrative, but only if you are armed with information and skills to take advantages of wealth-creating opportunities. Come to see us or call us to learn what you need to know to become a successful real estate investor. We are well equipped to assist you! |

| YOUR PATH TO WEALTH STARTS RIGHT NOW. JUST TAKE ACTION! It's a fact: today, anyone can become a millionaire – In the history of the world, there has never been a better time to create wealth than right here, right now in real estate. What if you could get some expert help? What if you could learn the wealth building techniques, strategies and secrets of investments ? What if you could learn directly from experience professional. WWW.KNOWLEDGEFINANCIAL.COM |

| start building your fortune – and make – our expertise, our competence, and our experience work for you? ''REAL ESTATE SERVICES'' SOUTH FLORIDA, PLEASE CONTACT ANTHONY. ----------------------------------------------------- Attaining wealth is the result of effort and making good decisions. Some of the decisions are major, However, they are all important. Where do you turn for sound advice when making a decision that involves money? You could get advice from a team of mortgage and real estate experts dedicated to your success? |

| REAL ESTATE FINANCING IS AVAILABLE FOR INVESTORS AT VISION MORTGAGE BANK. MORTGAGE HOME LOANS, HOME REFINANCING, HOME EQUITY IS JUST SIMPLE AND EASY. WE'RE HERE TO GUIDE YOU, TO INFORM YOU, AND WE HAVE GREAT DESIRE TO HELP YOU FIND THE BEST MORTGAGE PRODUCT AT THE LOWEST RATE POSSIBLE! FOR SOUTH FLORIDA |

| FLORIDA REAL ESTATE: HOME BUYING, HOME SELLING, RENTING, LISTING. PLEASE CALL US HELP IS AVAILABLE TO HELP YOU OR SOMEONE YOU KNOW SELL A PROPERTY. WE SELL FAST, QUICK AND FOR THE TOP PRICE. ---CONTACT ANTONY AN EXPERIENCED PROFESSIONAL REALTOR--- FORTUNE INT. REALTY. |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

KNOWLEDGEFINANCIAL.COM

| Ten Resolutions to Make Your Financial Life Easier KNOWLEDGEFINANCIAL.COM Another year gone by, and where did it go? If yours was anything like mine, it went far too fast. Now we have a new one right around the corner. In the interest of saving time, while attending to those pesky financial chores that must be done, here are some tips for making your financial life simpler (and richer) next year. Resolve to: 1. Pay bills at warp speed. About ten seconds is what it took me to pay a bill online that would have taken me at least a few minutes if I had to dig out my checkbook, write a check, slap on a stamp, and take it to a postbox. You can pay bills online. The research shows it’s likely safer than paying offline, as long as you keep your computer free of spyware and viruses. Setting up automatic withdrawals each month is even faster, since you don’t even have to log on for a bill to be paid. But be careful: I once had to fight to reverse an $851 withdrawal for an erroneous phone bill. I like to schedule automatic withdrawals only for bills with a fixed payment each month. For the rest of my bills, I go online to authorize before I allow any money to come out of my account. 2. Keep two credit cards, and freeze the rest. You might not be able to tile your pool with your plastic like Martha Stewart did in her television commercial a few years ago, but if you are a “typical” American, you own a wallet full of plastic. Two major credit cards should be all your need. Use more, and you might miss a due date and get hit with a painfully expensive late fee. Using one credit card with a low interest rate for purchases you won’t pay off in full, and one with no fee (plus rewards) for those you will should be enough. 3. Create a system. Whether it’s an online financial organizer like Mvelopes, Quicken, or Microsoft Money, or just something as simple as a filing drawer and notebook designated for your finances, find a place to organize your paperwork… and start doing it! You’ll save a bunch of time when you don’t have to dig through stacks of papers to find that receipt or cancelled check. Tax time will be a lot easier as well. 4. Start saving. If you haven’t had the time or energy to start a savings account, pick a method – any method -- and get started. Sign up to have a small amount transferred from your checking account to a savings or money market account each month; start spending only paper money and save your coins each day in a jar until you have enough to deposit in the bank; get a piggybank; or get a credit card that helps you save. It’s one resolution you definitely won’t regret. 5. Stop doing it all. The most successful people in business find good people to work for them, then delegate the things that are not the best use of their time or skills. They check in to make sure things are running smoothly, but they focus their energy on more important tasks. The same goes for your financial life. Your team can include a great accountant, insurance broker, and financial planner. Help them understand where you want to go, then let their expertise help you get there. 6. Sweat the big stuff. You have put it off long enough. It’s time to get your will, living will and/or estate plan set up. Update beneficiaries if you haven’t done so recently. Then make a list of all your accounts and passwords in case something should happen to you . Be sure you have enough life insurance to protect your loved ones. Hopefully you will have a good, healthy year. But if things don’t go as planned, you want those important items checked off your to-do list. 7. Go ahead, change your mind. Psychologists have been tackling the secrets of happiness , and guess what? After a certain point, it’s not about money. (And that point is usually around $50,000 a year, not a million). If you’re tired of worrying about money, then resolve that above all, you’ll be happy, regardless of your bank account balance. After all, what is life about, anyway? Fortunately, there are great tools now to help you change your mind. Anything by Martin Seligman, Ph.D., can help, and I also love The Prosperity Game , a free online game where you get to spend virtual checks on anything you want (with no bill due, ever!). 8. Save a few trees. Call 1-888-OPT-OUT and get your name taken off the mailing list for pre-approved credit offers. Then cut out more junk mail with tips from Good Advice Press . Like getting a good spam filter for your email, you’ll feel better when you walk to the mailbox and don’t face a mountain of unwanted ads. 9. Buy less. Stay away from the mall, turn off the TV, and if possible, get your kids to do the same. You’ll find a lot fewer temptations calling your name. Your bank account will be healthier, your home less cluttered, and you will free up time for the things you really enjoy. 10. Take it one step at a time. My favorite self-help book of the year, One Small Step Can Change Your Life by Robert Maurer, Ph.D. advises you to stop trying to make major changes and start with simple ones. Anything you can do in one minute or one action is ideal. So as you go through this list, don’t get overwhelmed. For example, if the thought of spending an afternoon setting up online bill payments gives you a headache, don’t take it one step at a time. Resolve to just set up one account online. Instead of agonizing over making our your will, make your first step only to ask three friends for referrals to an attorney who can help. Keep it simple. Enjoy yourself, and take things easy. Those are resolutions most of us can stick with. |

| METHODS AND TECHNIQUES TO HELP YOU REALLY OBTAIN AN ULTIMATE FINANCIAL FREEDOM! Retrain Your Brain to Cut Debt and Build Wealth Why is changing our behavior so difficult? Why do we get stuck in a rut so often? Why do we make dumb choices with our money that seem so obvious in hindsight? Recently, I’ve had the opportunity to delve into a couple of terrific psychology books, and I’d like to offer a few insights I’ve gleaned from them. The first, Why Smart People Make Big Money Mistakes and How to Correct Them, by Gary Belsky and Thomas Gilovich, focuses on research in behavioral finance. The book provides some fascinating insight to why our financial behaviors often just don’t make sense – and what we can do about it. Insight #1: It’s all in your head…and that’s the problem. One of the big dangers to wealth building is something called “mental accounting.” It describes how we allocate our money in our mind and how that translates into (often irrational) behavior. Mental accounting explains why we will handle a bonus or windfall differently than a pay raise, and especially why we treat plastic money (credit cards and debit cards) differently than cash, or money from a paycheck. (In case you haven’t heard, the research shows that generally consumers spend more when they pay with plastic, as compared to cash.) Belsky and Gilovich use the example of income tax refunds to illustrate how mental accounting works. While receiving a big tax refund once in a while might be a fluke, receiving a large refund year after year is ridiculous. “ Why lend the government your money for free?” ask financial advisors every April. But that’s because those who do get a tax refund often enjoy it as if it were “found money” and spent it as a windfall, instead as the deferral of salary that it really is. If we were to correctly adjust our withholding, for example, we would probably use the money from our larger paychecks more carefully, and be less likely to splurge on whatever it is we decide we really “need” when that big refund check arrives. They even describe one study where recipients of a relatively small amount of unexpected cash spent twice as much as they received. In Why Smart People Make Big Money Mistakes, the authors warn: “Mental accounting helps to explain one of the great puzzles of personal finance – why people who don’t see themselves as reckless spenders can’t seem to save enough. The devil, as they say, is in the details….Being cost-conscious when making little purchases is where you can often rack up big savings.” The pendulum can swing the other way, too. With mental accounting, investors can become too conservative with their money and fail to take the appropriate level of risk. Strategy: Write down every dollar you spend, large and small, for a month. Recording purchases as soon as you make them will keep your list accurate. Remember, you are trying to get away from the bias of mental accounting. At the end of the month, add up your spending in each category, and look for places where you make changes. An alternative: Cash your paycheck in small bills and use envelopes to hold the cash for each expense category. When the money is gone for the month, you stop spending in that category. Also smart: The authors also suggest another strategy: Wait. Park a windfall, tax refund, or other unexpected cash in a bank account for three to six months. After that time has passed, you are more likely to see the balance as savings, rather than extra money to spend on a whim. Insight #2: “Some of the more serious and costly financial mistakes people make are the result of inaction.” That insight from the chapter titled “The Devil That You Know,” isn’t news to me. After all, on many occasions I have talked to someone in a financial bind and offered my advice, only to find that they are back six month later, having taken no action and finding themselves in a worse situation than the first time we talked. But the research behind the phenomenon of “decision paralysis” was interesting. Belsky and Gilovich attribute it to a number of factors, including the fear of regretting our choices and a comfort level with the status quo (even when our current situation isn’ t so hot). Another reason for decision paralysis, however, is the myriad choices we have today. Need help getting out of debt? There are probably at least 2,500 different firms offering solutions. Need a mortgage? Well, there is the decision of what type of mortgage: interest-only, 2/28 ARM, 30-year fixed, or a hundred other varieties. Then there is also the decision of who to get the mortgage through: your local bank, a mortgage broker, an online company. Is it any wonder we are overwhelmed? The research shows that more choices are not necessarily good, and can lead to inaction. I’ve been there many times, and chances are, so have you. Strategy: Acknowledge the cost of inaction. Start investing and you may lose money. But don’t invest and I guarantee you won’t have anything. In other words, just because you can’t do everything you want to do financially doesn’t mean you can’t do anything at all. Starting a $5 per week investment account or adding an extra $5 a week to paying down your debt is better than nothing. Also smart: Identify the experts and get their advice. Sometimes it is hard to see your situation clearly when you are bogged down in it. An objective voice from someone who understands the options can be helpful, especially if you act upon it. You’ve come to a great place to start! You can browse the Credit.com learning center or choose a life stage to find information tailored to your situation. Insight #3: Small Changes Can Make a Big Difference. One Small Step Can Change Your Life by Robert Maurer, Ph.D., was another eye-opener for me. Dr. Maurer bases his book on the principal of kaizen, small incremental changes known for helping the Japanese develop a thriving industrial base after WWII. He encourages us to: Ask Small Questions Think Small Thoughts Take Small Actions Solve Small Problems Together, he says, these actions can create radical change (over time). They work, he explains, because our brain is hard-wired to resist change. Even the prospect of a change can trigger our fight- or-flight response, which in turn shuts down creativity and thinking. Small changes allow us to bypass that automatic response and succeed in changing. When Maurer talks about small change, he means small. Can’t exercise? Start with one minute of marching in front of the television. Overeating? Throw the first bite of chocolate, or one French fry, away (I am working on the chocolate one!). It sounds a bit ridiculous at first, but the idea is to help rewire the connections in your brain so that it enjoys your small successes, and doesn’t interfere as you try to build upon them. Strategy: Overspending? Put one item back when you reach the check out line. Can’t save? Start by saving one dollar from your paycheck, or one dollar a day. Having trouble getting out of debt? Each day, ask yourself one small question: What is one small action I can take to reduce my debt? Your brain loves questions, says Maurer, and by posing those small questions frequently, you will put it to work coming up with solutions. Also Smart: Forget the lottery or “all or nothing” mentality. Maurer says you don’t need (or perhaps don’t even want) a radical idea to be successful. The Japanese completely reinvented their economy and work style with the principal of kaizen…one very small step at a time. You can too. |

| HOME BUYING---- Let us help you purchase your property in the area you prefer for the price you can afford. Contact us to pre-qualify you first. Pre-qualification will put you in a stronger position to negotiate with sellers and become closer to reach an agreement on the purchase price |

| We’re here to turn traditional renters into property owners and landlords. We’ve great desire to help people find the right mortgage loan at the lowest rate possible. CALL Mr. ANTONY ---South Florida |

| We also specialize in Luxury Residential & waterfront properties. We have gained the reputation of great professional from some of the highest profile clients. We are raising the bar higher in customer service and playing a pivotal role in finding Finance for Real Estate. South Florida, CALL: -- |

| YOU NEED TO BUY OR LEASE A PROPERTY IN SOUTH FL. PLEASE. CONTACT US... COMMERCIAL, OR RESIDENTIAL FINANCIAL HELP IS AVAILABLE! FREE CREDIT REPAIR HELP FOR PROSPECT! |

| YOU’VE PROPERTY FOR SALE? CONTACT US COMMERCIAL, RESIDENTIAL, WE’LL BUY IT FROM YOU OR WE’LL SELL IT FOR YOU; FAST, QUICK & FOR THE TOP PRICE! SOUTH FLORIDA PLEASE CONTACT US… |

A licensed professional Realtor from Fortune

International Realty ------ or

an investor, who represents a Florida real estate

investment Corporation will contact you within 24 hour.

International Realty ------ or

an investor, who represents a Florida real estate

investment Corporation will contact you within 24 hour.

| | | | |

A step by step guide to gaining control

of your financial life.

Setting priorities

Here's help for the first -- and often the hardest -- step

in achieving your financial goals: deciding which goals

to pursue.

LESSON 2

Making a budget, saving money

How to bring your spending under control, so that you

get the most out of every dollar.

LESSON 3

Basics of banking and saving

Here's how to get the best banking services at the best

price, either online or off.

LESSON 4

Basics of investing

An introduction to making money in stocks, bonds and

mutual funds REIT'S, real estate.

LESSON 5

Investing in stocks

The market can be a great place to turn savings into

wealth -- or to lose your shirt. Here are some

fundamentals of investing wisely.

LESSON 6

Investing in mutual funds

It's a mutual-fund jungle out there. Here's how to create

a simple portfolio that works.

LESSON 7

Investing in bonds

Bonds can provide a steady and reasonably secure

income, while adding ballast to your portfolio--but only if

you really understand what you're buying.

LESSON 8

Buying a home

Owning your home is part of the American Dream, but if

you’re not prepared, buying it can be a nightmare. Here

are some fundamentals for buyers and sellers.

LESSON 9

Controlling debt

You've got to know when to hold debt--and when to fold

it. This lesson shows you how to accomplish your

financial goals by making debt work for you.

LESSON 10

Home Selling

WAYS TO SELL A PROPERTY FAST AND EASY FOR

THE TOP PRICE!

Selling a home is a big decision and requires a lot of

work. From getting the house ready to reviewing the

escrow papers, our helpful guide will walk you through

the process of selling your home.

INSURANCE

Health Insurance, Life Insurance, Home Insurance, Car

Insurance

Great things to know about insurance

Buying a car, Auto loans. Great things to know:

Buying a car is like no other shopping experience. The

choices seem to be endless. This lesson helps you

sort through your options.

FINANCIAL FREEDOM: A SMARTEST WAY TO PREPARE A

BETTER FUTURE. YOUR PATH TO WEALTH STARTS RIGHT

NOW.

It's a fact: today, anyone can become a millionaire

– In the history of the world, there has never been

a better time to create wealth than right here, right

now in real estate.

of your financial life.

Setting priorities

Here's help for the first -- and often the hardest -- step

in achieving your financial goals: deciding which goals

to pursue.

LESSON 2

Making a budget, saving money

How to bring your spending under control, so that you

get the most out of every dollar.

LESSON 3

Basics of banking and saving

Here's how to get the best banking services at the best

price, either online or off.

LESSON 4

Basics of investing

An introduction to making money in stocks, bonds and

mutual funds REIT'S, real estate.

LESSON 5

Investing in stocks

The market can be a great place to turn savings into

wealth -- or to lose your shirt. Here are some

fundamentals of investing wisely.

LESSON 6

Investing in mutual funds

It's a mutual-fund jungle out there. Here's how to create

a simple portfolio that works.

LESSON 7

Investing in bonds

Bonds can provide a steady and reasonably secure

income, while adding ballast to your portfolio--but only if

you really understand what you're buying.

LESSON 8

Buying a home

Owning your home is part of the American Dream, but if

you’re not prepared, buying it can be a nightmare. Here

are some fundamentals for buyers and sellers.

LESSON 9

Controlling debt

You've got to know when to hold debt--and when to fold

it. This lesson shows you how to accomplish your

financial goals by making debt work for you.

LESSON 10

Home Selling

WAYS TO SELL A PROPERTY FAST AND EASY FOR

THE TOP PRICE!

Selling a home is a big decision and requires a lot of

work. From getting the house ready to reviewing the

escrow papers, our helpful guide will walk you through

the process of selling your home.

INSURANCE

Health Insurance, Life Insurance, Home Insurance, Car

Insurance

Great things to know about insurance

Buying a car, Auto loans. Great things to know:

Buying a car is like no other shopping experience. The

choices seem to be endless. This lesson helps you

sort through your options.

FINANCIAL FREEDOM: A SMARTEST WAY TO PREPARE A

BETTER FUTURE. YOUR PATH TO WEALTH STARTS RIGHT

NOW.

It's a fact: today, anyone can become a millionaire

– In the history of the world, there has never been

a better time to create wealth than right here, right

now in real estate.

| WHAT GUIDELINES ARE REQUIRED FOR A MORTGAGE LOAN? Mortgages are used by individuals and businesses wishing to make large value purchase of real estate without payment the entire value of the purchase up front. Mortgages are also known as lien against property, or claims on property. Mortgage is a legal agreement that creates an interest in a real estate property between borrower and the lender. HOW TO UNDERSTAND THE HOME LOAN PROCESS? Understand that in order to finance or refinance a loan the lender requires documentation to verify and substantiate your employment, credit and financial situation to assure its investors that you have the ability to repay the MONEY HOME REFINANCING: 10 GREAT REASONS TO REFINANCE A PROPERTY. NOW IT'S THE BEST TIME FOR REFINANCING, THE INTEREST RATE IS VERY LOW. MORTGAGE LOAN MODIFICATION PROGRAMS; AN ALTERNATIVE TO REDUCE MONTHLY MORTGAGE PAYMENT, TO AVOID FORECLOSURE, TO SAVE YOUR CREDIT RATING, TO SAVE YOUR PROPERTY. REVERSE MORTGAGE NO MORTGAGE PAYMENTS EVER AGAIN: IF YOU OWNED A HOME AS YOUR PERSONAL RESIDENCE. TO IMPROVE YOUR QUALITY OF LIFE AND LIVE WITH NO STRESS! IF YOU'RE 62 YEARS OF AGE OR OLDER, YOU CAN ACHIEVE THIS, THROUGH A REVERSE MORTGAGE, REGULATED BY THE U.S. GOVERNMENT. FINANCING YOUR REAL ESTATE INVESTMENT; BUYING YOUR FIRST, SECOND, AND OR THIRD PROPERTY. HOW AND WHERE TO FIND MONEY? CLICK RIGHT HERE! FHA: F H A MORTGAGE LOANS, THE GOVERNMENT IS THERE TO HELP YOU PURCHASE YOUR HOME. PLEASE CONTACT US WE WILL SHOW YOU THE WAY . MORTGAGE LOAN PRE-QUALIFICATION, LOW INTEREST RATES, 8 Reasons to Get Pre-Approved for a Home Loan Learn why pre-approval is one of the smartest moves you can make when shopping for a home Subprime Mortgage  A type of mortgage that is normally made out to borrowers with lower credit ratings. As a result of the borrower's lowered credit rating, a conventional mortgage is not offered because the lender views the borrower as having a larger-than- average risk of defaulting on the loan. FINANCING YOUR REAL ESTATE INVESTMENT; BUYING YOUR FIRST, SECOND, AND OR THIRD PROPERTY. HOW AND WHERE TO FIND MONEY? CLICK RIGHT HERE! RENTAL PROPERTY / COMMERCIAL REAL ESTATE / COMMERCIAL LEASE Tips for Making Solid Business Agreements and Contracts |

| FORECLOSURE INVESTMENT The Time is Now to Profit from Foreclosure A “Perfect Storm” of events has made investing in foreclosure properties better than ever - and now’s the time for you to profit... THE HOME BUYING GUIDE!--------------------IMPORTANT THINGS TO KNOW BEFORE BUYING... The home-buying process doesn't need to be scary. Our step-by-step guide will walk you through the process and answer your questions on what you should expect from us as your realtor, where to look for loans, and what to watch out for when closing the deal. HOME SELLING: WAYS TO SELL A PROPERTY FAST AND EASY FOR THE TOP PRICE! Selling a home is a big decision and requires a lot of work. From getting the house ready to reviewing the escrow papers, our helpful guide will walk you through the process of selling your home. SHORT SALE: REAL ESTATE INVESTMENT OPPORTUNITY FOR ALL SHORT SALE allows you to buy as many properties as you want. Flip them, Hold them, Rent them, Refinance them and make profits. PRE-CONSTRUCTION, A GREAT WAY TO INVEST IN REAL ESTATE. BUT YOU HAVE TO KNOW THE SECRETS OF IT. Florida Real Estate for sale: Wonderful prices, great location,extraordinary view,very spacious. NO OTHER INVESTMENTS BUILD WEALTH LIKE REAL ESTATE! NOW REALLY IS A GREAT TIME TO BUY A PROPERTY: COMPETITIVE PRICES, LOW INTEREST RATES, MANY CHOICES COMMERCIAL REAL ESTATE; A BETTER WAY TO INVEST AND GET RICHER! MULTI-WAYS TO WIN BIG IN REAL ESTATE 1031 Exchange, Tax Saving Tips for Real Estate Investors and landlords Give Financial Advantage MIAMI REAL ESTATE: The Time is Now to Profit from Real Estate investing-- A “Perfect Storm” of events has made investing in Real Estate properties better than ever - and now’s the time for you to profit... CALL Mr. ANTONY AT: 786-709-6577 --- Fortune International Realty COMMERCIAL LEASE: Before you rent space for your business, be sure you understand these basic facts about commercial leases. Manufactured Homes, Mobile Homes, an Affordable Housing Alternative We are dedicated ourselves to helping bring prospective buyers of manufactured homes in contact with retailers who sell homes in their area. We aim to help buyers wade through the excess of information providing a simple directory that enables buyers to quickly and efficiently contact us to help them find the dealers in which they are interested. |

| ATTENTION, ATTENTION! IMPORTANT INFORMATION ABOUT THE UNITED STATES FIVE [5] BIGGEST FINANCIAL INSTITUTIONS... Bank of America Financial Services Wells Fargo Financial Services PNC-National City Mortgage Financial Services Citibank,Citifinancial, Citimortgage, Citigroup JPMorgan-Chase Financial Services ow to make the Bank say, "Yes You're p |

| -Financial Service Company. What We Do, How we do it? EVERYTHING YOU WANT TO KNOW ABOUT INSURANCE & INVESTMENT.- -How to Become Wealthy? Nine Truths That Can Set You on the Path to Financial Freedom-- -AMERICAN DOLLAR: What are the letters, numbers, and symbols, the latin words mean? -Money Management- Counterfeit Combat: Defense Is in the Details. How to reconize and combat counterfeit money? -'INVESTMENT & FINANCE: METHODS, TECHNIQUES, AND STRATEGIES. WHERE, WHEN, HOW TO INVEST? -Banking And Finance Knowledge. The more you know the closer you are to accomplish great success.. -The Role of Money in Our Life THE ARCHITECTURE OF PROSPERITY -RICH GUIDE: WHY AREN'T YOU RICH? BUILDING FINANCIAL WEALTH, OBTAIN FINANCIAL FREEDOM, BECOME A RICH PERSON; YES YOU CAN. -Ten Resolutions to Make Your Financial Life Easier- Counterfeit Combat: Defense Is in the Details... |

| IF YOU NEED HELP TO SELL YOUR REAL ESTATE PROPERTY IN SOUTH FLORIDA; PLEASE SOUTH FLORIDA, CALL ANTONY A PROFESSIONAL REALTOR. AT: 786-6317740 -- F. I. R.-- CLIENTS COMPLETE SATISFACTION GUARANTEED ! HOME-SELLING -- -REAL ESTATE SERVICES-- HOME-BUYING -REAL ESTATE INFO.-' -TIPS FOR HOME BUYERS - 10 Home Buying Mistakes To Avoid - |

| IF YOU NEED HELP TO SELL YOUR REAL ESTATE PROPERTY IN SOUTH FLORIDA; PLEASE CALL Mr. ANTONY A PROFESSIONAL REALTOR. ! HOME-SELLING -- -' -REAL ESTATE SERVICES-- HOME-BUYING -- REAL ESTATE INFO.---- MORTGAGE LOANS INFO. -- '' 'INVESTMENT & FINANCE: METHODS, TECHNIQUES, AND STRATEGIES. WHERE, WHEN, HOW TO INVEST? |

| ''-Life Insurance Options, Benefits, Advantages & Profits'' What You Really Need To Know ''-INSURANCE INFO / As an Insurance Representative, I'm Pride Myself in Delivering Excellence Service With Maximum Satisfaction . I Work Diligently to Provide Superior Products For A Minimum Cost.- CALL ANTHONY THE INSURANCE REPRESENTATIVE AT: 786-631-7740- Be Properly Protected With a Good Life Insurance Policy. Affordable Life Insurance: Best Price, Best Plan With The Best Company. South Florida, Call Anthony At: 786-631 -7740 ---- Family Treasure; Life Insurance Can be a Great One. |

'' 101 Ways To Make Money, Best Business Ideas

Ever Found On The Web To Become Financially

Secure. Path To Financial Freedom...

Are You Tired With A Job You Don't Like That

Much? Or Are You Exhausted Of Been

Unemployed?

Ever Found On The Web To Become Financially

Secure. Path To Financial Freedom...

Are You Tired With A Job You Don't Like That

Much? Or Are You Exhausted Of Been

Unemployed?

| ''Banking & Finance. The more you know the closer you are to financial success.- ''FREE QUOTE, FAST & EASY''''Find Out How Much You Can Save On Life Insurance- 'REQUEST A FREE QUOTE TODAY'' Find Out If You're Paying Too Much For Life Insurance. ''AFFORDABLE LIFE INSURANCE: BEST PRICES, BEST PLAN, WITH THE BEST COMPANY. SOUTH FL. CALL AT: 786-709-1531-- ''LIFE INSURANCE: Ways to Reduce Your Life Insurance Premium; ,,Insurance Products: How to make profits with the insurance companies? ; ;Term Insurance Is What? |

''Save Smartly, Invest Wisely''---KNOWLEDGEFINANCIAL.COM

Managing Money - Budget Basics

Creating a Budget Doesn't Have to be Hard

For most people, the word “budget” conjures up thoughts of penny-pinching and the

unpleasant task of crunching numbers. This couldn’t be further from the truth. A budget is at

the cornerstone of a solid financial foundation, regardless of your situation, and it isn’t that

hard to do.

What is a Budget?

A budget is nothing more than a breakdown and plan of how much money you have coming in

and where it goes. Could you imagine a business becoming successful if it didn’t keep track of

its income and expenses? The same holds true when it comes to your personal finances. If

you don’t know how much money you have coming in and where it goes, your road to financial

success will be a difficult one.

--------------------

How to Become Wealthy -----KNOWLEDGEFINANCIAL.COM

Ten{10} Truths That Can Set You on the Path to Financial Freedom

#1: Change the Way You Think About Money

The general population has a love / hate relationship with wealth. They resent those who have

it, but spend their entire lives attempting to get it for themselves. The reason a vast majority of

people never accumulate a substantial nest egg is because they don't understand the nature

of money or how it works.

Cash, like a person, is a living thing. When you wake up in the morning and go to work, you are

selling a product - yourself (or more specifically, your labor). When you realize that every morning your assets

wake up and have the same potential to work as you do, you unlock a powerful key in your life. Each dollar

you save is like an employee. Over the course of time, the goal is to make your employees work hard, and

eventually, they will make enough money to hire more workers (cash). When you have become truly

successful, you no longer have to sell your own labor, but can live off of the labor of your assets. At this time

you become financially independent.

#2: Develop an Understanding of the Power of Small Amounts

The biggest mistake most people make is that they think they have to start with an entire

Napoleon-like army. They suffer from the "not enough" mentality; namely that if they aren't

making $1,000 or $5,000 investments at a time, they will never become rich. What these

people don't realize is that entire armies are built one soldier at a time; so too is their financial

arsenal.

#3''With Each Dollar You Save, You Are Buying Yourself Freedom.

#4''You Are Responsible for Where You Are in Your Life

#5''Instead of Buying the Products only, made by the company... Buy

the Stocks of the company!

Someone once asked me why they weren't wealthy. They always felt like they were putting money aside, yet

never seemed to get any further ahead. The answer is simple. I told them to stop buying the products

companies sell and start buying the company itself!

#6''27-30% of all the income the wealthy earned went into investments

and savings. That isn't a result of being rich, that is why they are rich. When the pain of getting out of

the bondage of financial slavery is greater than the pain of changing your spending habits, you will become

rich. Either change, or be content to live as you are.

Managing Money - Budget Basics

Creating a Budget Doesn't Have to be Hard

For most people, the word “budget” conjures up thoughts of penny-pinching and the

unpleasant task of crunching numbers. This couldn’t be further from the truth. A budget is at

the cornerstone of a solid financial foundation, regardless of your situation, and it isn’t that

hard to do.

What is a Budget?

A budget is nothing more than a breakdown and plan of how much money you have coming in

and where it goes. Could you imagine a business becoming successful if it didn’t keep track of

its income and expenses? The same holds true when it comes to your personal finances. If

you don’t know how much money you have coming in and where it goes, your road to financial

success will be a difficult one.

--------------------

How to Become Wealthy -----KNOWLEDGEFINANCIAL.COM

Ten{10} Truths That Can Set You on the Path to Financial Freedom

#1: Change the Way You Think About Money

The general population has a love / hate relationship with wealth. They resent those who have

it, but spend their entire lives attempting to get it for themselves. The reason a vast majority of

people never accumulate a substantial nest egg is because they don't understand the nature

of money or how it works.

Cash, like a person, is a living thing. When you wake up in the morning and go to work, you are

selling a product - yourself (or more specifically, your labor). When you realize that every morning your assets

wake up and have the same potential to work as you do, you unlock a powerful key in your life. Each dollar

you save is like an employee. Over the course of time, the goal is to make your employees work hard, and

eventually, they will make enough money to hire more workers (cash). When you have become truly

successful, you no longer have to sell your own labor, but can live off of the labor of your assets. At this time

you become financially independent.

#2: Develop an Understanding of the Power of Small Amounts

The biggest mistake most people make is that they think they have to start with an entire

Napoleon-like army. They suffer from the "not enough" mentality; namely that if they aren't

making $1,000 or $5,000 investments at a time, they will never become rich. What these

people don't realize is that entire armies are built one soldier at a time; so too is their financial

arsenal.

#3''With Each Dollar You Save, You Are Buying Yourself Freedom.

#4''You Are Responsible for Where You Are in Your Life

#5''Instead of Buying the Products only, made by the company... Buy

the Stocks of the company!

Someone once asked me why they weren't wealthy. They always felt like they were putting money aside, yet

never seemed to get any further ahead. The answer is simple. I told them to stop buying the products

companies sell and start buying the company itself!

#6''27-30% of all the income the wealthy earned went into investments

and savings. That isn't a result of being rich, that is why they are rich. When the pain of getting out of

the bondage of financial slavery is greater than the pain of changing your spending habits, you will become

rich. Either change, or be content to live as you are.

#7'' Study and Admire Success and Those Who Have Achieved It...

Then Emulate ItA very wise investor once said to pick the traits you admire and dislike the most about your

heroes, then do everything in your power to develop the traits you like and reject the ones you don't. Mold

yourself into who you want to become. You'll find that by investing in yourself first, money will begin to flow

into your life. Success and wealth beget success and wealth. You have to purchase your way into that

cycle, and you do so by building your army one soldier at a time and putting your money to work for you.

#8''Realize that More Money is All Not the Answer, More money is not going to solve all your problems.

Money is a magnifying glass; it will accelerate and bring to light your true habits. If you are a good person

then it makes become abetter one but if you are a bad one, it assurely it could make you become the worst

one.

Mentality of a generation

Unless Your Parents Were Wealthy, Don't Do What They DidThe definition

of insanity is doing the same thing over and over again and expecting a different result. If your parents

were not living the life you want to live then don't do what they did! You must break away from the mentality

of past generations if you want to have a different lifestyle than they had.

To achieve the financial freedom and success that your family may or may not have had, you have to do

two things. First, make a firm commitment to get out of debt. To find out which debts should be paid off

before you invest and those that are acceptable, Second, make saving and investing the highest financial

priority in your life; one technique is to pay yourself first.

#9''Don't Worry--The miracle of life is that it doesn't matter so much

where you are,

it matters where you are going. Once you have made the choice to take control back of your life by building

up your net worth, don't give a second thought to the "what ifs".

Every moment that goes by, you are growing closer and closer to your ultimate goal - control and freedom.

Every dollar that passes through your hands is a seed to your financial future. Rest assured, if you are

diligent and responsible, financial prosperity is an inevitability.

The day will come when you make your last payment on your car, your house, or whatever else it is you

owe. Until then, enjoy the process.

How Much of My Money Should Stay In Safe Investments?

#10''You need to keep enough money in liquid, safe investments to

cover, at a minimum, three to six months worth of living expenses. This

means if you need $3,000 per month to live comfortably, you need to have $9,000 - $15,000 in safe, liquid

investments like bank savings accounts or money market funds.

•The less secure your employment, the more money you want to keep in safe investments.

•The closer you are to retirement, the more money you want to keep in safe investments.

#11'' Money Lessons Of Investment

Be Cautious Of Illiquid Investments

Illiquid investments are not bad investments, but you should be cautious. If you have too much money in

illiquid investments it can limit flexibility. Some examples are real estate partnerships, private placements,

private equity investments, non-publicly traded REITs .

Illiquid investments may offer higher returns. The trade off: you cannot easily cash them in.

Illiquid means that although you will not pay a penalty to get out of them, it may take months, or years, to

cash in your interest in the investment.

#12''Avoid Investments That You Don’t Understand

A good investment can turn into a bad investment when you don't understand how it works. When you lack

understanding or knowledge, you're more likely to make an illogical decision.

If it sounds complicated, or you just don’t understand the investment, do one of two things.

1.Ask more questions. (If someone isn’t willing to provide plain English answers, than walk away.)

2.Or, just walk away.

Then Emulate ItA very wise investor once said to pick the traits you admire and dislike the most about your

heroes, then do everything in your power to develop the traits you like and reject the ones you don't. Mold

yourself into who you want to become. You'll find that by investing in yourself first, money will begin to flow

into your life. Success and wealth beget success and wealth. You have to purchase your way into that

cycle, and you do so by building your army one soldier at a time and putting your money to work for you.

#8''Realize that More Money is All Not the Answer, More money is not going to solve all your problems.

Money is a magnifying glass; it will accelerate and bring to light your true habits. If you are a good person

then it makes become abetter one but if you are a bad one, it assurely it could make you become the worst

one.

Mentality of a generation

Unless Your Parents Were Wealthy, Don't Do What They DidThe definition

of insanity is doing the same thing over and over again and expecting a different result. If your parents

were not living the life you want to live then don't do what they did! You must break away from the mentality

of past generations if you want to have a different lifestyle than they had.

To achieve the financial freedom and success that your family may or may not have had, you have to do

two things. First, make a firm commitment to get out of debt. To find out which debts should be paid off

before you invest and those that are acceptable, Second, make saving and investing the highest financial

priority in your life; one technique is to pay yourself first.

#9''Don't Worry--The miracle of life is that it doesn't matter so much

where you are,

it matters where you are going. Once you have made the choice to take control back of your life by building

up your net worth, don't give a second thought to the "what ifs".

Every moment that goes by, you are growing closer and closer to your ultimate goal - control and freedom.

Every dollar that passes through your hands is a seed to your financial future. Rest assured, if you are

diligent and responsible, financial prosperity is an inevitability.

The day will come when you make your last payment on your car, your house, or whatever else it is you

owe. Until then, enjoy the process.

How Much of My Money Should Stay In Safe Investments?

#10''You need to keep enough money in liquid, safe investments to

cover, at a minimum, three to six months worth of living expenses. This

means if you need $3,000 per month to live comfortably, you need to have $9,000 - $15,000 in safe, liquid

investments like bank savings accounts or money market funds.

•The less secure your employment, the more money you want to keep in safe investments.

•The closer you are to retirement, the more money you want to keep in safe investments.

#11'' Money Lessons Of Investment

Be Cautious Of Illiquid Investments

Illiquid investments are not bad investments, but you should be cautious. If you have too much money in

illiquid investments it can limit flexibility. Some examples are real estate partnerships, private placements,

private equity investments, non-publicly traded REITs .

Illiquid investments may offer higher returns. The trade off: you cannot easily cash them in.

Illiquid means that although you will not pay a penalty to get out of them, it may take months, or years, to

cash in your interest in the investment.

#12''Avoid Investments That You Don’t Understand

A good investment can turn into a bad investment when you don't understand how it works. When you lack

understanding or knowledge, you're more likely to make an illogical decision.

If it sounds complicated, or you just don’t understand the investment, do one of two things.

1.Ask more questions. (If someone isn’t willing to provide plain English answers, than walk away.)

2.Or, just walk away.

#14''Don’t Put All Your Money in the Same Type of

Investment --KNOWLEDGEFINANCIAL.COM

Anyone who recommends you put ALL of your money in any of the following investments is

giving you bad investment advice.

•Annuities – Annuities can offer guarantees that may be important to you. However, if someone

recommends you put all your money, both taxable money and tax deferred money (such as IRA

accounts), into annuities, this is not wise.

•REIT’s – A REIT is a Real Estate Investment Trust,

like a mutual fund that owns real estate, usually commercial or retail real estate. Some REIT’s

are great investments. However, when I see a client who has put their entire IRA account, for

example, into a single REIT, this is not a wise move.

•Tax Deferred Accounts – You want to build a balance between tax deferred

accounts (such as IRA or 401k accounts) and after tax money. If all your money is in tax

deferred accounts, it can come back to hurt you.

#14''Ways A Custodian Protects You From Investment Fraud

Investment Fraud And Rogue Advisors Can Be Avoided By Using A Custodian

There is one simple, almost sure-fire way, to prevent investment fraud .

Use only investment advisors that use large, reputable custodians to handle your assets.

Reduced Opportunity For Investment Fraud

Since your investment advisor does not have custody of your assets this means they never

directly handle your checks, deposits, or withdrawals. This reduces the opportunity for fraud.

When an investment advisor uses a custodian although the advisor can direct withdrawals to

be made, those withdrawals must be direct deposited to another account of yours, or sent by

check to your address on file.

Ask The Following 4 Questions To Avoid Investment Fraud

1.Who is the custodian of my assets?

2.What type of fraud detection technology does the

custodian have in place?

3.What type of insurance does the custodian provide if fraud

does occur?

4.Who generates my account statements?--------------------

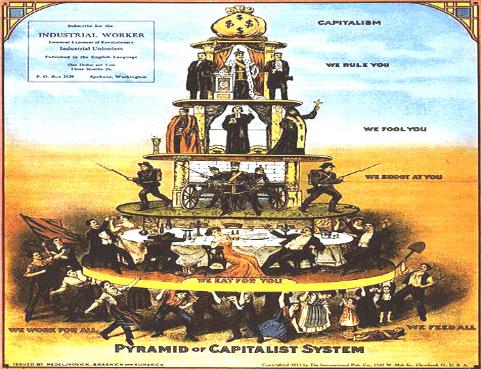

Secrets of the Capitalist Class

They Diversify Income Sources as Well as Assets, a big

different between rich and poor: the rich invest their income

and spend thes rest; the poor spend their income and invest

the rest. nothing really left to invest.

The Capitalist Class Prefers Passive Income Over Active

Income

Passive income can come from sources as varied as:

•Rent from real estate properties

•Patent royalties for an invention

•Trademark licensing fees for characters or brands you’ve created

•Royalties from books, songs, publications, or other original works

•Profits from businesses in which you have little or no day-to-day role or

responsibility

•Earnings from Internet advertisements on a blog or website you own

•Dividends from stocks, REITs, equity mutual funds, or other equity securities

•Interest from owning bonds, certificates of deposit, other other cash and cash

equivalents

•Pensions

•Residual income for a sales person on accounts that are typically renewed

automatically such as a sporting goods representative that earns a commission

on his accounts, bringing in a few thousand dollars per store per year for simply

servicing the customers once they have been opened

KNOWLEDGEFINANCIAL.COM

Investment --KNOWLEDGEFINANCIAL.COM

Anyone who recommends you put ALL of your money in any of the following investments is

giving you bad investment advice.

•Annuities – Annuities can offer guarantees that may be important to you. However, if someone

recommends you put all your money, both taxable money and tax deferred money (such as IRA

accounts), into annuities, this is not wise.

•REIT’s – A REIT is a Real Estate Investment Trust,

like a mutual fund that owns real estate, usually commercial or retail real estate. Some REIT’s

are great investments. However, when I see a client who has put their entire IRA account, for

example, into a single REIT, this is not a wise move.

•Tax Deferred Accounts – You want to build a balance between tax deferred

accounts (such as IRA or 401k accounts) and after tax money. If all your money is in tax

deferred accounts, it can come back to hurt you.

#14''Ways A Custodian Protects You From Investment Fraud

Investment Fraud And Rogue Advisors Can Be Avoided By Using A Custodian

There is one simple, almost sure-fire way, to prevent investment fraud .

Use only investment advisors that use large, reputable custodians to handle your assets.

Reduced Opportunity For Investment Fraud

Since your investment advisor does not have custody of your assets this means they never

directly handle your checks, deposits, or withdrawals. This reduces the opportunity for fraud.

When an investment advisor uses a custodian although the advisor can direct withdrawals to

be made, those withdrawals must be direct deposited to another account of yours, or sent by

check to your address on file.

Ask The Following 4 Questions To Avoid Investment Fraud

1.Who is the custodian of my assets?

2.What type of fraud detection technology does the

custodian have in place?

3.What type of insurance does the custodian provide if fraud

does occur?

4.Who generates my account statements?--------------------

Secrets of the Capitalist Class

They Diversify Income Sources as Well as Assets, a big

different between rich and poor: the rich invest their income

and spend thes rest; the poor spend their income and invest

the rest. nothing really left to invest.

The Capitalist Class Prefers Passive Income Over Active

Income

Passive income can come from sources as varied as:

•Rent from real estate properties

•Patent royalties for an invention

•Trademark licensing fees for characters or brands you’ve created

•Royalties from books, songs, publications, or other original works

•Profits from businesses in which you have little or no day-to-day role or

responsibility

•Earnings from Internet advertisements on a blog or website you own

•Dividends from stocks, REITs, equity mutual funds, or other equity securities

•Interest from owning bonds, certificates of deposit, other other cash and cash

equivalents

•Pensions

•Residual income for a sales person on accounts that are typically renewed

automatically such as a sporting goods representative that earns a commission

on his accounts, bringing in a few thousand dollars per store per year for simply

servicing the customers once they have been opened

KNOWLEDGEFINANCIAL.COM

| The Capitalist Class Understands the Nature of Money ----KNOWLEDGEFINANCIAL.COM The poor and working class see money as a finite commodity; there is only so much and then you spend it until there is none left. The rich members of the capitalist class know the truth: Money is like a seed. The same principles that farmers have been using regarding sewing and reaping to provide food for thousands of years hold fast for money. Each dollar that comes in to your hand has the potential to be planted, grow, and expand into far more money. It's no different than a farmer growing corn. You can either eat your seed, or plant your seed. One gives you satisfaction today; the other can feed your family for generations. The Capitalist Class Doesn't Care What the Market Does. They always ready to take advantage of it, buy low sell high. The great warrent buffet said: Be greedy when others are fearful and be fearful when others are greedy''! The Capitalist Class Understands Taxes The average person doesn't bother to read the tax rules or pay to have good accountants. It is more than possible to save substantially on taxes by learning the regulations the IRS makes available in easy to download documents on the official website. The Capitalist Class Thinks of Business as a Game The middle class often has an almost perverse relationship with money. From the time students leave college, they are told to get a good, "secure" job with benefits, fear stock market fluctuations, and spend their money on assets that depreciate such as cars and consumer electronics. For the capitalist class, business and money are merely tokens - tangible proof that they have succeeded. The Capitalist Class Realizes Money is a Fungible Commodity A defining characteristic of the capitalist class is that they treat money as a fungible commodity. This manifests itself in several ways. •Members of the capitalist class don't care if they earn their profits from non-sexy businesses such as trash hauling, storage units, or plumbing services. The middle class often does care by treating family members that are lawyers or doctors with more respect because of how they earn their money. •When raising capital to start or expand a business, members of the capitalist class don't care where the money comes from, only the terms and cost of the funds. They will often approach banks, private equity groups, or even insurance companies! The middle class heads to one, or maybe two, local banks and if the answer is "no", simply stops trying. •The capitalist class doesn't compartmentalize money like the middle class does. Members of the middle class who are drowning in credit card debt will often use unexpected bonuses or tax rebates for vacations or other perks. The capitalist class sees every dollar as a dollar and puts it toward its greatest use. |

| ..Life Insurance Advantages, Benefits, & Features While Alive and After Death... Learn More Here! ..Insurance General Information: Ways to Make Money & Save Money on Your Insurance. Learn More... ..Term Insurance Advantages, Term Insurance General Knowledge. Buy the Term, and invest the difference. Learn More... ..Life Insurance Quote. Find out if You Pay too much for Your Insurance, Or Check How Much You Can Pay For a Life Insurance... ..Investment Products: Investing & Money Management Basics. FINANCIAL SOLUTIONS, TOOLS & RESOURCES. LEARN MORE... Insurance Products: How to make profits with the insurance companies? Learn More... INSURANCE 101: THE IMPORTANCE OF INSURANCE IN SOMEONE'S LIFE. EVERYTHING YOU NEED TO KNOW ABOUT INSURANCE; LEARN HOW TO SAVE MONEY ON YOUR INSURANCE! LEARN ABOUT THE [5] fIVE MOST IMPORTANT INSURANCE |

''Exchange Traded Funds (ETFs) Discover exchange traded funds and learn how to make

them a profitable part of your portfolio.

''THE RULES OF SUCCESS, AND THE NEW RULE OF MONEY.-

them a profitable part of your portfolio.

''THE RULES OF SUCCESS, AND THE NEW RULE OF MONEY.-

| -New Rules of Money- The Rules of Money: How to Make It, and How to Hold on to It - Basic Money Rules That Could Make You Change Your Life Financially-- Learn More..- |

| ''KNOWLEDGE: 'Finance and Investment Knowledge Research Invention And Discovery. Saving and Investing - Financial Knowledge, Financial Literacy, Financial Education And Resources For All. -- ''AMERICAN BANKING SYSTEM: BANKING HISTORY; GREAT THINGS TO KNOW ABOUT THE AMERICAN BANKING HISTORY BANKING AND FINANCE, COMMERCIAL BANKING: The fundamental functions of a commercial bank during the past two centuries SAVING: THE SECRETS OF SAVING; WAYS TO SAVE A LOT OF MONEY AND GETTING RICHER. 66 WAYS TO SAVE MONEY MONEY MANAGEMENT: Ten Resolutions to Make Your Financial Life Easier. 10 Ways to Avoid Overdraft and Bounced Check Fees ''INDEX FUNDS -What You Need to Know About Trading and Investing in Leveraged ETFs. What Does Index Fund Mean?- ''MONEY: '45 Ways to Improve Your Finances This Year. Whether you want to ramp up your earning power, finally start a retirement savings account. -- '' Market Advice Plus The Definition Of The Financial Terms: ''Financial Freedom Strategies Methods And techniques to win. Financial Freedom,the ways to obtain, Look for them, find them and take action! Path to financial independence '' RETIREMENT: SOCIAL SECURITY; THE ULTIMATE RETIREMENT GUIDE. HOW DOES SOCIAL SECURITY WORK? Does someone can depend only on Social Security check? ''SAVING MONEY: THE SECRETS OF SAVING; WAYS TO SAVE A LOT OF MONEY AND GETTING RICHER '' RULES OF SUCCESS, RULES OF MONEY: THE RULES OF SUCCESS-The rules of money have changed and it’s time for you to get smart with your money! -- THE 16 DAYS THAT SHOOCK THE US ECONOMY IN SEPTEMBER, 2008. A shocking series of events that forever changed the financial markets. AMERICA’S MONEY CRISIS / Bailout 101: What new law says. Here's a rundown of key provisions of the financial rescue plan that United State Senate voted, Wednesday October 1; and the house voted Friday October 3, 2008. FORTUNE, CREATION AND INTRODUCTION: When you invest in stock, you buy ownership shares in a company. Before You Invest; Before undertaking any investment program, it is critical that you assess your current situation and form goals. Evaluating a Stock, Creating an Emergency Fund Trust Account: Definition of a Trust; Land Trust, Living Trust, Revocable Trust. In general, a "trust" is a legal entity that is able to own property and other assets. -- |

'' 101 Ways To Make Money,

Best Business Ideas Ever

Found On The Web To

Become Financially Secure.

Path To Financial Freedom...

Are You Tired With A Job

You Don't Like That Much?

Or Are You Exhausted Of

Been Unemployed? Get Help

Here!-

Best Business Ideas Ever

Found On The Web To

Become Financially Secure.

Path To Financial Freedom...

Are You Tired With A Job

You Don't Like That Much?

Or Are You Exhausted Of

Been Unemployed? Get Help

Here!-

| '' 101 Ways To Make Money, Best Business Ideas Ever Found On The Web To Become Financially Secure. Path To Financial Freedom... Are You Tired With A Job You Don't Like That Much? Or Are You Exhausted Of Been Unemployed? Get Help Here!- |

| ''A Life Insurance Plan Is Available For Every Wallet; Low Cost Premium, Very Affordable Plan With A Great Company. For More Info, South FL. CALL ANTHONY <Be Properly Protected With a Good Life Insurance Policy> Available At Very Low Rates, -''Child Term Rider Every Kids Cover Under Parents, ''Disability Waiver of Premium In Case You Become Disable, No More Payments. ''No physical exam required *** EXCELLENT LIFE INSURANCE PLAN: BEST PRICES, WITH THE BEST COMPANY. LEARN MORE.. CALL A REPRESENTATIVE - |