ARTICLES/BUILDING WEALTH

How to Become Wealthy?

Nine Truths That Can Set

You on the Path to

Financial Freedom

#1: Change the Way You Think

About Money

understand the nature of money or how it works.

understand the nature of money or how it works.

Cash, like a person, is a living thing. When you wake up in the morning and go

to work, you are selling a product - yourself (or more specifically, your labor).

When you realize that every morning your assets wake up and have the same

potential to work as you do, you unlock a powerful key in your life. Each dollar

you save is like an employee.

Over the course of time, the goal is to make your employees work hard, and

eventually, they will make enough money to hire more workers (cash). When

you have become truly successful, you no longer have to sell your own labor,

but can live off of the labor of your assets.

#2: Develop an

Understanding of the

Power of Small Amounts

The biggest mistake most people make is that they think they have to start with

an entire Napoleon-like army. They suffer from the "not enough" mentality;

namely that if they aren't making $1,000 or $5,000 investments at a time, they

will never become rich. What these people don't realize is that entire armies

are built one soldier at a time; so too is their financial arsenal.

#3: With Each Dollar You Save,

You Are Buying Yourself

Freedom

When you put it in these terms, you see how spending $20 here and $40 there

can make a huge difference in the long run. Since money has the ability to

work in your place, the more of it you employ, the faster and larger it will grow.

Along with more money comes more freedom - the freedom to stay home with

your kids, the freedom to retire and travel around the world, or the freedom to

quit your job. If you have any source of income, it is possible for you to start

building wealth today. It may only be $5 or $10 at a time, but each of those

investments is a stone in the foundation of your financial freedom.

#4: You Are Responsible for

Where You Are in Your Life

Years ago, a friend told me she didn't want to invest in stocks because she

"didn't want to wait ten years to be rich..." she would rather enjoy her money

now. The folly with this school of thinking is that the odds are, you are going

to be alive in ten years. The question is whether or not you will be better off

when you arrive there. Where you are right now is the sum total of the

decisions you have made in the past. Why not set the stage for your life in the

future right now?

#5: Instead of Buying the

Product... Buy the Stock!

Someone once asked me why they weren't wealthy. They always felt like they

were putting money aside, yet never seemed to get any further ahead. The

answer is simple. I told them to stop buying the products companies sell and

start buying the company itself! A survey of America's affluent (those who

make over $225,000 a year or own $3,000,000 in assets) revealed that 27-30%

of all the income the wealthy earned went into investments and savings.

That isn't a result of being rich, that is why they are rich. When the pain of

getting out of the bondage of financial slavery is greater than the pain of

changing your spending habits, you will become rich. Either change, or be

content to live as you are.

#6: Study and Admire Success

and Those Who Have Achieved

It... Then Emulate It

A very wise investor once said to pick the traits you admire and dislike the

most about your heroes, then do everything in your power to develop the traits

you like and reject the ones you don't. Mold yourself into who you want to

become.

You'll find that by investing in yourself first, money will begin to flow into your

life. Success and wealth beget success and wealth. You have to purchase

your way into that cycle, and you do so by building your army one soldier at a

time and putting your money to work for you.

#7: Realize that More Money is

Not the Answer

More money is not going to solve your problem. Money is a magnifying glass;

it will accelerate and bring to light your true habits. If you are not capable of

handling a job paying $18,000 a year, the worst possible thing that could

happen to you is for you to earn six figures. It would destroy you. I have met

too many people earning $100,000 a year who are living from paycheck to

paycheck and don't understand why it is happening. The problem isn't the size

of their checkbook, it is the way in which they were taught to use money.

#8: Unless Your Parents Were

Wealthy, Don't Do What They

Did

The definition of insanity is doing the same thing over and over again and

expecting a different result. If your parents were not living the life you want to

live then don't do what they did! You must break away from the mentality of

past generations if you want to have a different lifestyle than they had.

To achieve the financial freedom and success that your family may or may

not have had, you have to do two things. First, make a firm commitment to get

out of debt. To find out which debts should be paid off before you invest and

those that are acceptable, read Pay Off Your Debt or Invest?. Second, make

saving and investing the highest financial priority in your life; one technique

is to pay yourself first.

Purchasing equity is vital to your financial success as an individual whether

you are in need of cash income or desire long-term appreciation in stock

value. Nowhere else can your money do as much for you as when you use it to

invest in a business that has wonderful long-term prospects.

#9: Don't Worry

The miracle of life is that it doesn't matter so much where you are, it matters

where you are going. Once you have made the choice to take control back of

your life by building up your net worth, don't give a second thought to the

"what ifs". Every moment that goes by, you are growing closer and closer to

your ultimate goal - control and freedom.

Every dollar that passes through your hands is a seed to your financial future.

Rest assured, if you are diligent and responsible, financial prosperity is an

inevitability. The day will come when you make your last payment on your

car, your house, or whatever else it is you owe. Until then, enjoy the process.

Nine Truths That Can Set

You on the Path to

Financial Freedom

#1: Change the Way You Think

About Money

understand the nature of money or how it works.

understand the nature of money or how it works.

Cash, like a person, is a living thing. When you wake up in the morning and go

to work, you are selling a product - yourself (or more specifically, your labor).

When you realize that every morning your assets wake up and have the same

potential to work as you do, you unlock a powerful key in your life. Each dollar

you save is like an employee.

Over the course of time, the goal is to make your employees work hard, and

eventually, they will make enough money to hire more workers (cash). When

you have become truly successful, you no longer have to sell your own labor,

but can live off of the labor of your assets.

#2: Develop an

Understanding of the

Power of Small Amounts

The biggest mistake most people make is that they think they have to start with

an entire Napoleon-like army. They suffer from the "not enough" mentality;

namely that if they aren't making $1,000 or $5,000 investments at a time, they

will never become rich. What these people don't realize is that entire armies

are built one soldier at a time; so too is their financial arsenal.

#3: With Each Dollar You Save,

You Are Buying Yourself

Freedom

When you put it in these terms, you see how spending $20 here and $40 there

can make a huge difference in the long run. Since money has the ability to

work in your place, the more of it you employ, the faster and larger it will grow.

Along with more money comes more freedom - the freedom to stay home with

your kids, the freedom to retire and travel around the world, or the freedom to

quit your job. If you have any source of income, it is possible for you to start

building wealth today. It may only be $5 or $10 at a time, but each of those

investments is a stone in the foundation of your financial freedom.

#4: You Are Responsible for

Where You Are in Your Life

Years ago, a friend told me she didn't want to invest in stocks because she

"didn't want to wait ten years to be rich..." she would rather enjoy her money

now. The folly with this school of thinking is that the odds are, you are going

to be alive in ten years. The question is whether or not you will be better off

when you arrive there. Where you are right now is the sum total of the

decisions you have made in the past. Why not set the stage for your life in the

future right now?

#5: Instead of Buying the

Product... Buy the Stock!

Someone once asked me why they weren't wealthy. They always felt like they

were putting money aside, yet never seemed to get any further ahead. The

answer is simple. I told them to stop buying the products companies sell and

start buying the company itself! A survey of America's affluent (those who

make over $225,000 a year or own $3,000,000 in assets) revealed that 27-30%

of all the income the wealthy earned went into investments and savings.

That isn't a result of being rich, that is why they are rich. When the pain of

getting out of the bondage of financial slavery is greater than the pain of

changing your spending habits, you will become rich. Either change, or be

content to live as you are.

#6: Study and Admire Success

and Those Who Have Achieved

It... Then Emulate It

A very wise investor once said to pick the traits you admire and dislike the

most about your heroes, then do everything in your power to develop the traits

you like and reject the ones you don't. Mold yourself into who you want to

become.

You'll find that by investing in yourself first, money will begin to flow into your

life. Success and wealth beget success and wealth. You have to purchase

your way into that cycle, and you do so by building your army one soldier at a

time and putting your money to work for you.

#7: Realize that More Money is

Not the Answer

More money is not going to solve your problem. Money is a magnifying glass;

it will accelerate and bring to light your true habits. If you are not capable of

handling a job paying $18,000 a year, the worst possible thing that could

happen to you is for you to earn six figures. It would destroy you. I have met

too many people earning $100,000 a year who are living from paycheck to

paycheck and don't understand why it is happening. The problem isn't the size

of their checkbook, it is the way in which they were taught to use money.

#8: Unless Your Parents Were

Wealthy, Don't Do What They

Did

The definition of insanity is doing the same thing over and over again and

expecting a different result. If your parents were not living the life you want to

live then don't do what they did! You must break away from the mentality of

past generations if you want to have a different lifestyle than they had.

To achieve the financial freedom and success that your family may or may

not have had, you have to do two things. First, make a firm commitment to get

out of debt. To find out which debts should be paid off before you invest and

those that are acceptable, read Pay Off Your Debt or Invest?. Second, make

saving and investing the highest financial priority in your life; one technique

is to pay yourself first.

Purchasing equity is vital to your financial success as an individual whether

you are in need of cash income or desire long-term appreciation in stock

value. Nowhere else can your money do as much for you as when you use it to

invest in a business that has wonderful long-term prospects.

#9: Don't Worry

The miracle of life is that it doesn't matter so much where you are, it matters

where you are going. Once you have made the choice to take control back of

your life by building up your net worth, don't give a second thought to the

"what ifs". Every moment that goes by, you are growing closer and closer to

your ultimate goal - control and freedom.

Every dollar that passes through your hands is a seed to your financial future.

Rest assured, if you are diligent and responsible, financial prosperity is an

inevitability. The day will come when you make your last payment on your

car, your house, or whatever else it is you owe. Until then, enjoy the process.

| 7 Rules of Wealth Building Practical Keys to Amassing Investment Capital Most parents want to teach their children responsibility - how to become self sufficient and succeed in life (after all, no one plans on raising a dead beat). However, very few actually accomplish this task. Why? Because, as parents, we are limited to the experiences our parents passed on to us; the antiquated notion that "responsibility" is simply getting a job, saving a little money, and maybe purchasing a car or some equally important item. Hopefully these seven rules will open your eyes and help you teach your children to avoid the traps that have stolen financial success from so many people. Wealth Building Rule 1: Put Off Marriage Your biggest obstacle to attaining wealth is YOU. Too often, people live their lives in a manner that is not conducive to creating riches and then get frustrated at "the system" when they only really have themselves to blame. One of the most important financial decisions you will ever make is marriage (more specifically who you marry and when). By putting off the walk down the aisle for a few years, you can save a decade worth of frustration. ---knowledgefinancial.com Your first goal should be to become financially independent, with little or no debt, and have your investments in place. Once you have these three things, your odds of success are drastically improved by beginning your journey on a level playing field (after all, the number-one reason for divorce is financial trouble). Wealth Building Rule 2: Debt is a Disease With a few notable exceptions, debt is a form of bondage; a disease that enslaves the borrower. A few years ago, there was a young lady attending college who shot herself because she couldn't pay back $2,300 in credit card debt. Although an extreme example, it is a testament to the power money has over peoples' lives. Imagine your life without owing anyone anything; your car, your house, your education, all paid for in full. Like what you see? When you want it badly enough, you will make extinguishing your debt your number one priority. Wealth Building Rule 3:----knowledgefinancial.com If You Don't Like Where your Parents Were at Your Age - Do Things Differently The old cliché that "insanity is doing the same thing over and over expecting different results," holds just as true today as it did when it was originally written. If you don't like where your parents were at your age, stop what you are doing. During your childhood, they taught you all they knew about money. For many people, these early years established how they feel about their finances today. In order to become financially successful, you must do something different than they did. Otherwise, you will end up exactly as they are. Wealth Building Rule 4: When you Begin a Job, Look at the Pay of the Highest Employee Whether you are looking for employment now or are thinking about it sometime in the near future, one of the most important things for you to do is to look at what the top-dog gets at any company for which you are considering working. This will give you an idea of how high you can expect to climb in terms of earnings and promotion. If the CEO is making $30,000 a year, you have no chance to make six figures. Select a job accordingly. Wealth Building Rule 5:----knowledgefinancial.com Do Something You Love and Get Paid for It I remember going into college and being surrounded with people who wanted to be artists, scientists, and businessmen, but instead did what their parents or grandparents told them to do. There is no honor in being a doctor or a lawyer if you wake up every morning and hate your job. Pick a profession you love and you'll never have to work a day in your life. Wealth Building Rule 6: Understand the Money Myth Money is nothing more than a piece of paper with the image of a long-dead person on it. When you understand that any power it has over you is derived from your relationship with it, you suddenly become free from the constant pressures and stress of thinking about it. Especially at times such as these, if you are putting money away for ten, fifteen, or twenty years down the road, stop checking your portfolio every day! There is nothing you can gain from it except stress. Wealth Building Rule 7: knowledgefinancial.com Your New Commodity is Not Your Labor, It's Your Ideas With the advent of the Internet and other technological advances, you are no longer limited to supporting yourself or making a living by your physical labor. The only limit you have on yourself now is your own imagination - your ideas are the most valuable thing you possess. Every man, woman, and child is a salesman for a living; if you don't own a business or investments, then you sell your manual labor to a company in exchange for a paycheck Change your product. The gap between the rich and poor does indeed grow larger with each passing year, but not because of inequalities or any other such injustices. Instead, it is because the rich understand money and how to use it. Capital is literally a seed; learn how to plant it to produce the best harvest. When you do this, you will rule your finances, not the other way around. |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

BUILDING WEALTH // Outrageous New-Car Scams To Avoid

How to Become Wealthy?

Nine Truths That Can Set You on the Path to Financial Freedom.

Becoming Wealthy One Bite at a Time!

7 Rules of Wealth Building

Practical Keys to Amassing Investment Capital-----------CLICK BELOW, GO DOWN BELOW...

How to Become Wealthy?

Nine Truths That Can Set You on the Path to Financial Freedom.

Becoming Wealthy One Bite at a Time!

7 Rules of Wealth Building

Practical Keys to Amassing Investment Capital-----------CLICK BELOW, GO DOWN BELOW...

KNOWLEDGEFINANCIALGROUP.COM

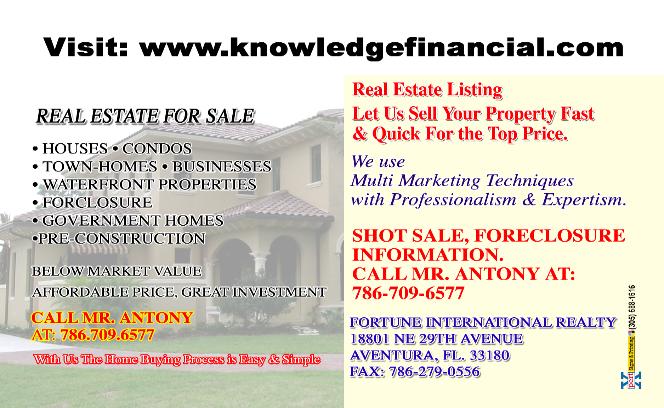

| YOU NEED TO BUY, OR LEASE A PROPERTY IN SOUTH FL. --- PLEASE CONTACT US... COMMERCIAL, OR RESIDENTIAL |

A licensed professional Realtor from Fortune International or

an investor, who represents a Florida real estate investment

Corporation will contact you within 24 hour.

--------------------------------------------------------------------------------

an investor, who represents a Florida real estate investment

Corporation will contact you within 24 hour.

--------------------------------------------------------------------------------

| ATTENTION SELLERS: LET US SELL YOUR PROPERTY FOR YOU FAST, QUICK, & FOR THE TOP PRICE. WITH US: IS MORE EXPOSURE, MORE SHOWINGS, MORE OFFERS, & MORE MONEY FOR YOUR PROPERTY. CALL: 786- |

| YOU’VE PROPERTY FOR SALE? CONTACT US COMMERCIAL, Or RESIDENTIAL WE’LL BUY IT FROM YOU OR WE’LL SELL IT FOR YOU; FAST, QUICK & FOR THE TOP PRICE! SOUTH FLORIDA PLEASE CONTACT US… |

| | | | |

Banking and Finance, Business and Financial

news, Political News, The Market News.

THE BANKING AND THE AMERICAN FINANCIAL

SYSTEM. HISTORY, SUCCESS AND FAILURE!

SMALL BUSINESS, METHODS, TECHNIQUES,

AND STRATEGIES

Business structures 101. LLP, LLC, S-corp and

C-corp: It's not just alphabet soup! A breakdown

of what you need to know, in layman's terms.

FINANCIAL KNOWLEDGE: The Successful

Investment Journey, Ten Tips For The

Successful Long-Term Investor. Ten Steps to

Building a Winning Trading Plan, Five Things To

Know About Asset Allocation

SAVING MONEY: THE SECRETS OF SAVING;

WAYS TO SAVE A LOT OF MONEY AND GETTING

RICHER. 66 WAYS TO SAVE MONEY

BUILDING WEALTH! How to Become Wealthy?

Nine Truths That Can Set You on the Path to

Financial Freedom.

Becoming Wealthy One Bite at a Time! 7 Rules of

Wealth Building, Practical Keys to Amassing

Investment Capital

UNCLAIMED MONEY, UNCLAIMED PROPERTY,

THE FORGOTTEN TREASURE SEATING IN THE

HANDS OF THE STATES GOVERNMENT

COULD BE YOURS OR TO SOMEONE YOU MAY

KNOW!

Billions of dollars have been lost. Could some of

it be yours? Yes the government may owed

you money; you may not even know about it.

FINANCIAL FREEDOM: A SMARTEST WAY TO

PREPARE A BETTER FUTURE IS TO PLAN TODAY

TO OBTAIN A COMPLETE FINANCIAL FREEDOM.

Ten Resolutions to Make Your Financial Life

Easier

WHY YOU AREN’T RICH?

Many people assume they aren't rich because

they don't earn enough money. If I only earned a

little more, I could save and invest better, they

say, they don’t have a good education, they say

they have too much responsibilities; Excuses,

Excuses, Excuses. THIS IS WHY!

INSURANCE: WAYS TO MAKE MONEY & SAVE

MONEY ON YOUR INSURANCE. THE

IMPORTANCE OF INSURANCE IN SOMEONE'S

LIFE!

Homeowners' Insurance: What You Need to

Know. Auto Insurance, Life Insurance

Will & Living trust

What is a will and what is living trust? How

does a living trust avoid probate?

Auto Loans: Great Car, Great Price…. But what

about the Financing? Explore your financing

options!---

Auto dealers have a long history of using

questionable sales tactics to bilk consumers in

the market for a new car. Many people keep

their eye on the sale price and neglect scams

involving vehicle financing, which can add

thousands of dollars to the price of a car.

Money Management: 10 Ways to Avoid

Overdraft and Bounced Check Fees! Three Ways

to Put Your Budget On on Auto Pilot! The Low

Tech Way to Budget Your Money

FREE CREDIT REPORT CAN HELP YOU FIND OUT

WHAT'S GOOD OR WHAT'S BAD AND ALSO

DETECT ID THEFT!

CREDIT INFO: SAVE YOUR CREDIT, RESCUE IT,

PROTECT IT, INCREASE YOUR SCORE. WE

HAVE VALUABLE INFORMATION TO HELP YOU.

IDENTITY THEFT: HOW TO PROTECT AND

DEFEND YOURSELF AGAINST IDENTITY

THEFT? -----DETER, DETECT AND DEFEND?

DEFEND YOURSELF AGAINST IDENTITY THEFT;

LEARN THE IMPORTANT METHODS AND

TECHNIQUES TO RECOVER FROM ID THEFT!

news, Political News, The Market News.

THE BANKING AND THE AMERICAN FINANCIAL

SYSTEM. HISTORY, SUCCESS AND FAILURE!

SMALL BUSINESS, METHODS, TECHNIQUES,

AND STRATEGIES

Business structures 101. LLP, LLC, S-corp and

C-corp: It's not just alphabet soup! A breakdown

of what you need to know, in layman's terms.

FINANCIAL KNOWLEDGE: The Successful

Investment Journey, Ten Tips For The

Successful Long-Term Investor. Ten Steps to

Building a Winning Trading Plan, Five Things To

Know About Asset Allocation

SAVING MONEY: THE SECRETS OF SAVING;

WAYS TO SAVE A LOT OF MONEY AND GETTING

RICHER. 66 WAYS TO SAVE MONEY

BUILDING WEALTH! How to Become Wealthy?

Nine Truths That Can Set You on the Path to

Financial Freedom.

Becoming Wealthy One Bite at a Time! 7 Rules of

Wealth Building, Practical Keys to Amassing

Investment Capital

UNCLAIMED MONEY, UNCLAIMED PROPERTY,

THE FORGOTTEN TREASURE SEATING IN THE

HANDS OF THE STATES GOVERNMENT

COULD BE YOURS OR TO SOMEONE YOU MAY

KNOW!

Billions of dollars have been lost. Could some of

it be yours? Yes the government may owed

you money; you may not even know about it.

FINANCIAL FREEDOM: A SMARTEST WAY TO

PREPARE A BETTER FUTURE IS TO PLAN TODAY

TO OBTAIN A COMPLETE FINANCIAL FREEDOM.

Ten Resolutions to Make Your Financial Life

Easier

WHY YOU AREN’T RICH?

Many people assume they aren't rich because

they don't earn enough money. If I only earned a

little more, I could save and invest better, they

say, they don’t have a good education, they say

they have too much responsibilities; Excuses,

Excuses, Excuses. THIS IS WHY!

INSURANCE: WAYS TO MAKE MONEY & SAVE

MONEY ON YOUR INSURANCE. THE

IMPORTANCE OF INSURANCE IN SOMEONE'S

LIFE!

Homeowners' Insurance: What You Need to

Know. Auto Insurance, Life Insurance

Will & Living trust

What is a will and what is living trust? How

does a living trust avoid probate?

Auto Loans: Great Car, Great Price…. But what

about the Financing? Explore your financing

options!---

Auto dealers have a long history of using

questionable sales tactics to bilk consumers in

the market for a new car. Many people keep

their eye on the sale price and neglect scams

involving vehicle financing, which can add

thousands of dollars to the price of a car.

Money Management: 10 Ways to Avoid

Overdraft and Bounced Check Fees! Three Ways

to Put Your Budget On on Auto Pilot! The Low

Tech Way to Budget Your Money

FREE CREDIT REPORT CAN HELP YOU FIND OUT

WHAT'S GOOD OR WHAT'S BAD AND ALSO

DETECT ID THEFT!

CREDIT INFO: SAVE YOUR CREDIT, RESCUE IT,

PROTECT IT, INCREASE YOUR SCORE. WE

HAVE VALUABLE INFORMATION TO HELP YOU.

IDENTITY THEFT: HOW TO PROTECT AND

DEFEND YOURSELF AGAINST IDENTITY

THEFT? -----DETER, DETECT AND DEFEND?

DEFEND YOURSELF AGAINST IDENTITY THEFT;

LEARN THE IMPORTANT METHODS AND

TECHNIQUES TO RECOVER FROM ID THEFT!

Read the most popular monthly News Letter

---CLICK HERE

Financial News, Business News, Market News.--

and 11 Great things to Do With Your Money in

Financial Crisis, in Difficult Economic Time!

Banking and Finance; Top online banking service

and solution for everyone

Click Here to see the most advanced electronic

products with the recent technology

Building Wealth, How to create a fortune.

American Banking System and History

Personal Finance, Us Financial System

How to obtain a complete and absolute Freedom

Financial Knowledge, get the knowledge you need

to succeed financially

Saving Money, 66 ways to save a lot of money

US Economy, Pension Plans retire early, retire rich

INVESTING / METHODS AND TECHNIQUES TO

INVEST IN TODAY'S MARKET FOR A BETTER

TOMORROW

Business, Easy ways to create your own

business. How to buy and sell a franchise?

Shop all you want right here; reliable, safe and

secure website. Best products from the world top

manufacturers, excellent prices

CLICK HERE ---TO SEE THE WOLD LARGEST

INTERNET BUSINESSES, THE HIGHEST QUALITY

MERCHANDISE FROM THE MOST SOPHISTICATED

COMPANIES

---CLICK HERE

Financial News, Business News, Market News.--

and 11 Great things to Do With Your Money in

Financial Crisis, in Difficult Economic Time!

Banking and Finance; Top online banking service

and solution for everyone

Click Here to see the most advanced electronic

products with the recent technology

Building Wealth, How to create a fortune.

American Banking System and History

Personal Finance, Us Financial System

How to obtain a complete and absolute Freedom

Financial Knowledge, get the knowledge you need

to succeed financially

Saving Money, 66 ways to save a lot of money

US Economy, Pension Plans retire early, retire rich

INVESTING / METHODS AND TECHNIQUES TO

INVEST IN TODAY'S MARKET FOR A BETTER

TOMORROW

Business, Easy ways to create your own

business. How to buy and sell a franchise?

Shop all you want right here; reliable, safe and

secure website. Best products from the world top

manufacturers, excellent prices

CLICK HERE ---TO SEE THE WOLD LARGEST

INTERNET BUSINESSES, THE HIGHEST QUALITY

MERCHANDISE FROM THE MOST SOPHISTICATED

COMPANIES

| ..Life Insurance Advantages, Benefits, & Features While Alive and After Death... Learn More Here! ..Insurance General Information: Ways to Make Money & Save Money on Your Insurance. Learn More... ..Term Insurance Advantages, Term Insurance General Knowledge. Buy the Term, and invest the difference. Learn More... ...Investment Products: Investing & Money Management Basics. FINANCIAL SOLUTIONS, TOOLS & RESOURCES. LEARN MORE... Insurance Products: How to make profits with the insurance companies? Learn More... |

| --FREE SCHOLARSHIP FOR SCHOOL-- ''FREE GOVERNMENT GRANTS MONEY FOR SCHOOL-- --LOW INTEREST RATE LOANS FROM THE NATION LARGEST SOURCES OF LOCAL, NATIONAL, SPECIFIC SCHOLARSHIP AMERICAN DOLLAR. What are the letters, numers, and symbols, the latin words, the glowing eyes mean? BUILDING WEALTH RICH GUIDE: WHY AREN'T YOU RICH? BUILDING FINANCIAL WEALTH, OBTAIN FINANCIAL FREEDOM, BECOME A RICH PERSON; YES YOU CAN... Learn More! Financial Education - Financial Knowledge Everything You Need To Know About Finance. Dubai- The World Largest, Biggest, Tallest, Greatest of Almost Everything. Learn more about this magnificent place and as well as other countries. COPYRIGHT-- What is Copyright? The Basics About Copyright Registration. The procedure for copyright registration. Do I need copyright protection? How do I register? Learn More! ''AUTO LOANS: Great Car, Great Price…. but what about the Financing? Explore your financing options! Five Tips for Getting the Best Deal On a Car... AUTO DEALERSHIP: 5 Car Dealer Extras You May Not Need, Or You Don't Need... Before buying a car; learn this first... ..News Letter: Tax Saving Business News, financial news, the world market. ..Biography & History of the world greatest personalities & politicians,, ..The world worst natural disasters & earthquakes in the history of humanity,, .Inventions. Great Inventions and discoveries of the century,, What are they? .. HAITI: Things you don't know & what you must know. Learn More!,, ..Life Insurance Advantages, Benefits, & Features While Alive and After Death... Learn More Here! ..Insurance General Information: Ways to Make Money & Save Money on Your Insurance. Learn More... ..Term Insurance Advantages, Term Insurance General Knowledge. Buy the Term, and invest the difference. Learn More... ...Investment Products: Investing & Money Management Basics. FINANCIAL SOLUTIONS, TOOLS & RESOURCES. LEARN MORE... Insurance Products: How to make profits with the insurance companies? Learn More... |

IF YOU NEED HELP TO SELL YOUR PROPERTY; PLEASE

CALL Mr. ANTONY A PROFESSIONAL REALTOR. - --- F. Int.

Realty. ---

-REAL ESTATE SERVICES-- HOME-BUYING -- REAL ESTATE

INFO.---- Home Selling -// Commercial Real Estate..

CALL Mr. ANTONY A PROFESSIONAL REALTOR. - --- F. Int.

Realty. ---

-REAL ESTATE SERVICES-- HOME-BUYING -- REAL ESTATE

INFO.---- Home Selling -// Commercial Real Estate..

10 PLACES NOT RECOMMENDED TO USE

DEBIT CARDS:

Debit cards have different protections and uses. Sometimes

they're not the best choice.

Sometimes reaching for your wallet is like a multiple choice

test: How do you really want to pay?

More from KNOWLEDGEFINANCIALGROUP.COM:

While credit cards and debit cards may look almost identical,

not all plastic is the same.

Consumers need to be particularly careful during vacation

season because identity thieves come out in droves. That

makes it pivotal that consumers keep their debit cards on ice,

said Beth Givens, director of the Privacy Rights Clearing House

and one of the nation's foremost experts on keeping your

private information private.

What makes debit cards so dangerous? Givens has so many

reasons, her organization has put out an exhaustive fact sheet

on whether you should use cash, credit or debit cards when

shopping. (The report also explains the shortcomings of gift

cards.)

Here's the short version of the dangers of debit:

------------------------------------------------

The Dangers of Using a Debit Card.

---knowledgefinancialgroup.com

"It's important that consumers understand the difference

between a debit card and a credit card," says John Breyault,

director of the Fraud Center for the National Consumers

League, a Washington, D.C.-based advocacy group. "There's a

difference in how the transactions are processed and the

protections offered to consumers when they use them."

While debit cards and credit cards each have advantages, each

is also better suited to certain situations. And since a debit card

is a direct line to your bank account, there are places where it

can be wise to avoid handing it over -- if for no other reason

than complete peace of mind.

-----------------------------------------

Here are 10 places and situations where it can

pay to leave that debit card in your wallet:

1. Online----- NOT TO USE

----KNOWLEDGEFINANCIALGROUP.COM

"You don't use a debit card online," says Susan Tiffany, director

of consumer periodicals for the Credit Union National

Association. Since the debit card links directly to a checking

account, "you have potential vulnerability there," she says.

Her reasoning: If you have problems with a purchase or the

card number gets hijacked, a debit card is "vulnerable because

it happens to be linked to an account," says Linda Foley,

founder of the Identity Theft Resource Center. She also includes

phone orders in this category.

The Federal Reserve's Regulation E (commonly dubbed Reg E),

covers debit card transfers. It sets a consumer's liability for

fraudulent purchases at $50, provided they notify the bank

within two days of discovering that their card or card number

has been stolen. KNOWLEDGEFINANCIALGROUP.COM

Most banks have additional voluntary policies that set their own

customers' liability with debit cards at $0, says Nessa Feddis,

vice president and senior counsel for the American Bankers

Association.

But the protections don't relieve consumers of hassle: The

prospect of trying to get money put back into their bank

account, and the problems that a lower-than-expected balance

can cause in terms of fees and refused checks or payments,

make some online shoppers reach first for credit cards.

2. Big-Ticket Items---- NOT TO USE

With a big ticket item, a credit card is safer, says Chi Chi Wu,

staff attorney with the National Consumer Law Center. A credit

card offers dispute rights if something goes wrong with the

merchandise or the purchase, she says.

"With a debit card, you have fewer protections,"

KNOWLEDGEFINANCIALGROUP.COM

In addition, some cards will also offer extended warrantees.

And in some situations, such as buying electronics or renting a

car, some credit cards also offer additional property insurance

to cover the item.

Two caveats, says Wu. Don't carry a balance. Otherwise, you

also risk paying some high-ticket interest. And "avoid store

cards with deferred interest," Wu advises.

3. Deposit Required------- NOT TO USE

That way, the store has its security deposit, and you still have

access to all of the money in your bank account. With any luck,

you'll never actually have to part with a dollar.

4. Restaurants--- NOT TO USE -----

knowledgefinancialgroup.com

"To me, it's dangerous," "You have so many people around."

Foreman bases his conclusions on what he hears from

readers. "Anecdotally, the cases that I'm hearing of credit or

debit information being stolen, as often as not, it's in a

restaurant," he says.

The danger: Restaurants are one of the few places where you

have to let cards leave your sight when you use them. But

others think that avoiding such situations is not workable.

The "conventional advice of 'don't let the card out of your sight'

-- that's just not practical," says Tiffany.

The other problem with using a debit card at restaurants: Some

establishments will approve the card for more than your

purchase amount because, presumably, you intend to leave a

tip.

So the amount of money frozen for the transaction could be

quite a bit more than the amount of your tab. And it could be a

few days before you get the cash back in your account.

5. You're a New Customer------ NOT TO USE

------knowledgefinancial.com

Online or in the real world, if you're a first-time customer in a

store, skip the debit card the first couple of times you buy,

That way, you get a feel for how the business is run, how you're

treated and the quality of the merchandise before you hand

over a card that links to your checking account.

6. Buy Now, Take Delivery Later-- NOT TO USE

Buying now but taking delivery days or weeks from now? A

credit card offers dispute rights that a debit card typically does

not.

"It may be an outfit you're familiar with and trust, but something

might go wrong," says Breyault, "and you need protection."

But be aware that some cards will limit the protection to a

specific time period, says Feddis. So settle any problems as

soon as possible.

7. Recurring Payments

We've all heard the urban legend about the gym that won't stop

billing an ex-member's credit card. Now imagine the charges

aren't going onto your card, but instead coming right out of your

bank account.

Another reason not to use the debit card for recurring charges:

your own memory and math skills. Forget to deduct that

automatic bill payment from your checkbook one month, and

you could either face fees or embarrassment (depending on

whether you've opted to allow overdrafting or not).

So if you don't keep a cash buffer in your account, "to protect

yourself from over-limit fees, you may want to think about using

a credit card" for recurring payments.

8. Future Travel-----NOT TO USE

----knowledgefinancialgroup.com

Book your travel with a check card, and "they debit it

immediately," So if you're buying travel that you won't use for

six months or making a reservation for a few weeks from now,

you'll be out the money immediately.

Another factor that bothers a lot of people: Hotels aren't

immune to hackers and data breaches, and several

name-brand establishments have suffered the problem

recently.

Do you want your debit card information "to sit in a system for

four months, waiting for you to arrive?" she asks. "I would not."

9. Gas Stations and Hotels---- NOT TO USE

This one depends on the individual business. Some gas

stations and hotels will place holds to cover customers who

may leave without settling the entire bill. That means that even

though you only bought $10 in gas, you could have a temporary

bank hold for $50 to $100. KNOWLEDGEFINANCIALGROUP.COM

Ditto hotels, where there are sometimes holds or deposits in

the hundreds to make sure you don't run up a long distance bill,

empty the mini bar or trash the room. The practice is almost

unnoticeable if you're using credit, but can be problematic if

you're using a debit card and have just enough in the account to

cover what you need.

At hotels, ask about deposits and holds before you present your

card, says Feddis. At the pump, select the pin-number option,

she says, which should debit only the amount you've actually

spent.

10. Checkouts or ATMs That Look 'Off'--- NOT TO USE

Criminals are getting better with skimmers and planting them in

places you'd never suspect -- like ATM machines on bank

property, says Foley.

So take a good look at the machine or card reader the next time

you use an ATM or self-check lane, she advises. Does the

machine fit together well or does something look

off.---KNOWLEDGEFINANCIALGROUP.COM

DEBIT CARDS:

Debit cards have different protections and uses. Sometimes

they're not the best choice.

Sometimes reaching for your wallet is like a multiple choice

test: How do you really want to pay?

More from KNOWLEDGEFINANCIALGROUP.COM:

While credit cards and debit cards may look almost identical,

not all plastic is the same.

Consumers need to be particularly careful during vacation

season because identity thieves come out in droves. That

makes it pivotal that consumers keep their debit cards on ice,

said Beth Givens, director of the Privacy Rights Clearing House

and one of the nation's foremost experts on keeping your

private information private.

What makes debit cards so dangerous? Givens has so many

reasons, her organization has put out an exhaustive fact sheet

on whether you should use cash, credit or debit cards when

shopping. (The report also explains the shortcomings of gift

cards.)

Here's the short version of the dangers of debit:

------------------------------------------------

The Dangers of Using a Debit Card.

---knowledgefinancialgroup.com

"It's important that consumers understand the difference

between a debit card and a credit card," says John Breyault,

director of the Fraud Center for the National Consumers

League, a Washington, D.C.-based advocacy group. "There's a

difference in how the transactions are processed and the

protections offered to consumers when they use them."

While debit cards and credit cards each have advantages, each

is also better suited to certain situations. And since a debit card

is a direct line to your bank account, there are places where it

can be wise to avoid handing it over -- if for no other reason

than complete peace of mind.

-----------------------------------------

Here are 10 places and situations where it can

pay to leave that debit card in your wallet:

1. Online----- NOT TO USE

----KNOWLEDGEFINANCIALGROUP.COM

"You don't use a debit card online," says Susan Tiffany, director

of consumer periodicals for the Credit Union National

Association. Since the debit card links directly to a checking

account, "you have potential vulnerability there," she says.

Her reasoning: If you have problems with a purchase or the

card number gets hijacked, a debit card is "vulnerable because

it happens to be linked to an account," says Linda Foley,

founder of the Identity Theft Resource Center. She also includes

phone orders in this category.

The Federal Reserve's Regulation E (commonly dubbed Reg E),

covers debit card transfers. It sets a consumer's liability for

fraudulent purchases at $50, provided they notify the bank

within two days of discovering that their card or card number

has been stolen. KNOWLEDGEFINANCIALGROUP.COM

Most banks have additional voluntary policies that set their own

customers' liability with debit cards at $0, says Nessa Feddis,

vice president and senior counsel for the American Bankers

Association.

But the protections don't relieve consumers of hassle: The

prospect of trying to get money put back into their bank

account, and the problems that a lower-than-expected balance

can cause in terms of fees and refused checks or payments,

make some online shoppers reach first for credit cards.

2. Big-Ticket Items---- NOT TO USE

With a big ticket item, a credit card is safer, says Chi Chi Wu,

staff attorney with the National Consumer Law Center. A credit

card offers dispute rights if something goes wrong with the

merchandise or the purchase, she says.

"With a debit card, you have fewer protections,"

KNOWLEDGEFINANCIALGROUP.COM

In addition, some cards will also offer extended warrantees.

And in some situations, such as buying electronics or renting a

car, some credit cards also offer additional property insurance

to cover the item.

Two caveats, says Wu. Don't carry a balance. Otherwise, you

also risk paying some high-ticket interest. And "avoid store

cards with deferred interest," Wu advises.

3. Deposit Required------- NOT TO USE

That way, the store has its security deposit, and you still have

access to all of the money in your bank account. With any luck,

you'll never actually have to part with a dollar.

4. Restaurants--- NOT TO USE -----

knowledgefinancialgroup.com

"To me, it's dangerous," "You have so many people around."

Foreman bases his conclusions on what he hears from

readers. "Anecdotally, the cases that I'm hearing of credit or

debit information being stolen, as often as not, it's in a

restaurant," he says.

The danger: Restaurants are one of the few places where you

have to let cards leave your sight when you use them. But

others think that avoiding such situations is not workable.

The "conventional advice of 'don't let the card out of your sight'

-- that's just not practical," says Tiffany.

The other problem with using a debit card at restaurants: Some

establishments will approve the card for more than your

purchase amount because, presumably, you intend to leave a

tip.

So the amount of money frozen for the transaction could be

quite a bit more than the amount of your tab. And it could be a

few days before you get the cash back in your account.

5. You're a New Customer------ NOT TO USE

------knowledgefinancial.com

Online or in the real world, if you're a first-time customer in a

store, skip the debit card the first couple of times you buy,

That way, you get a feel for how the business is run, how you're

treated and the quality of the merchandise before you hand

over a card that links to your checking account.

6. Buy Now, Take Delivery Later-- NOT TO USE

Buying now but taking delivery days or weeks from now? A

credit card offers dispute rights that a debit card typically does

not.

"It may be an outfit you're familiar with and trust, but something

might go wrong," says Breyault, "and you need protection."

But be aware that some cards will limit the protection to a

specific time period, says Feddis. So settle any problems as

soon as possible.

7. Recurring Payments

We've all heard the urban legend about the gym that won't stop

billing an ex-member's credit card. Now imagine the charges

aren't going onto your card, but instead coming right out of your

bank account.

Another reason not to use the debit card for recurring charges:

your own memory and math skills. Forget to deduct that

automatic bill payment from your checkbook one month, and

you could either face fees or embarrassment (depending on

whether you've opted to allow overdrafting or not).

So if you don't keep a cash buffer in your account, "to protect

yourself from over-limit fees, you may want to think about using

a credit card" for recurring payments.

8. Future Travel-----NOT TO USE

----knowledgefinancialgroup.com

Book your travel with a check card, and "they debit it

immediately," So if you're buying travel that you won't use for

six months or making a reservation for a few weeks from now,

you'll be out the money immediately.

Another factor that bothers a lot of people: Hotels aren't

immune to hackers and data breaches, and several

name-brand establishments have suffered the problem

recently.

Do you want your debit card information "to sit in a system for

four months, waiting for you to arrive?" she asks. "I would not."

9. Gas Stations and Hotels---- NOT TO USE

This one depends on the individual business. Some gas

stations and hotels will place holds to cover customers who

may leave without settling the entire bill. That means that even

though you only bought $10 in gas, you could have a temporary

bank hold for $50 to $100. KNOWLEDGEFINANCIALGROUP.COM

Ditto hotels, where there are sometimes holds or deposits in

the hundreds to make sure you don't run up a long distance bill,

empty the mini bar or trash the room. The practice is almost

unnoticeable if you're using credit, but can be problematic if

you're using a debit card and have just enough in the account to

cover what you need.

At hotels, ask about deposits and holds before you present your

card, says Feddis. At the pump, select the pin-number option,

she says, which should debit only the amount you've actually

spent.

10. Checkouts or ATMs That Look 'Off'--- NOT TO USE

Criminals are getting better with skimmers and planting them in

places you'd never suspect -- like ATM machines on bank

property, says Foley.

So take a good look at the machine or card reader the next time

you use an ATM or self-check lane, she advises. Does the

machine fit together well or does something look

off.---KNOWLEDGEFINANCIALGROUP.COM

..Sexuality-- Love Connection-- Relationship-- Free Dating

Sites.--- Personal ---- Family Adult Positions

Sites.--- Personal ---- Family Adult Positions

..Sexuality-- Love Connection-- Relationship-- Free Dating Sites.---

Personal ---- Family Adult Positions

Personal ---- Family Adult Positions

''NURSING EDUCATION CENTER- JOBS,

SCHOOLS, TRAINING, FINANCIAL AID. Nursing

News, Nursing Events,

-FREE SCHOLARSHIP FOR SCHOOL--

''FREE GOVERNMENT GRANTS MONEY FOR

SCHOOL-- --LOW INTEREST RATE LOANS FROM

THE NATION LARGEST SOURCES

AMERICAN DOLLAR. What are the letters, numers,

and symbols, the latin words, the glowing eyes

mean?

BUILDING WEALTH

RICH GUIDE: WHY AREN'T YOU RICH? BUILDING

FINANCIAL WEALTH, OBTAIN FINANCIAL

FREEDOM, BECOME A RICH PERSON; YES YOU

CAN... Learn More!

Financial Education - Financial Knowledge

Everything You Need To Know About Finance.

''AUTO LOANS: Great Car, Great Price…. But what

about the Financing? Explore your financing

options!

Five Tips for Getting the Best Deal On a Car...

AUTO DEALERSHIP: 5 Car Dealer Extras You May

Not Need, Or You Don't Need... Before buying a

car; learn this first...

Banking, Finance: The more you know the closer

you are to accomplish great success.

Business, Financial, Commercial News &

Commentary ..

SCHOOLS, TRAINING, FINANCIAL AID. Nursing

News, Nursing Events,

-FREE SCHOLARSHIP FOR SCHOOL--

''FREE GOVERNMENT GRANTS MONEY FOR

SCHOOL-- --LOW INTEREST RATE LOANS FROM

THE NATION LARGEST SOURCES

AMERICAN DOLLAR. What are the letters, numers,

and symbols, the latin words, the glowing eyes

mean?

BUILDING WEALTH

RICH GUIDE: WHY AREN'T YOU RICH? BUILDING

FINANCIAL WEALTH, OBTAIN FINANCIAL

FREEDOM, BECOME A RICH PERSON; YES YOU

CAN... Learn More!

Financial Education - Financial Knowledge

Everything You Need To Know About Finance.

''AUTO LOANS: Great Car, Great Price…. But what

about the Financing? Explore your financing

options!

Five Tips for Getting the Best Deal On a Car...

AUTO DEALERSHIP: 5 Car Dealer Extras You May

Not Need, Or You Don't Need... Before buying a

car; learn this first...

Banking, Finance: The more you know the closer

you are to accomplish great success.

Business, Financial, Commercial News &

Commentary ..

| ATTENTION SELLERS: CALL ANTONY AT: LET US HELP YOU SELLING YOUR PROPERTY. WITH US: IS MORE ADVERTISEMENT, MORE EXPOSURE, MORE SHOWINGS, MORE OFFERS, AND MORE MONEY FOR YOUR PROPERTY! CALL: 786- --- SOUTH FLORIDA. --- WE,RE LICENSED REALTOR & LICENSED MORTGAGE |

CANADA USA REAL

ESTATE!

HOW TO BUY REAL IN

SOUTH FLORIDA?

Home-buying & Selling

Guide For All Canadians

ESTATE!

HOW TO BUY REAL IN

SOUTH FLORIDA?

Home-buying & Selling

Guide For All Canadians

''INSURANCE-- Everything You Need to Know About Insurance; South Florida, Call The Insurance Representative At: -

- Get an Insurance Quote, Look How much a Policy Can Cost You, or See If You're Paying Too Much For a Policy.-- Get

a Quote!--

#1-10 PLACES NOT RECOMMENDED TO USE DEBIT CARDS:-- Financial Freedom.-- Seven Rules of Wealth Building

Keys to Amassing Investment Capital...

,, Start your own business EASY & SIMPLE, be your own boss, make extra money, secure your financial future,

obtain financial freedom.

- Get an Insurance Quote, Look How much a Policy Can Cost You, or See If You're Paying Too Much For a Policy.-- Get

a Quote!--

#1-10 PLACES NOT RECOMMENDED TO USE DEBIT CARDS:-- Financial Freedom.-- Seven Rules of Wealth Building

Keys to Amassing Investment Capital...

,, Start your own business EASY & SIMPLE, be your own boss, make extra money, secure your financial future,

obtain financial freedom.

Start your own business EASY & SIMPLE, be your own boss, make extra money, secure your financial

future, obtain financial freedom. LEARN MORE! CLICK HERE..

future, obtain financial freedom. LEARN MORE! CLICK HERE..

ADDITIONAL INFORMATION ABOUT

THE DANGER OF DEBIT/CREDIT

CARDS!

The Dangers of Using a

Debit Card. ---knowledgefinancial.com ----

PLACES AND WAYS NOT

RECOMMENDED TO USE

DEBIT CARDS:

Consumers need to be particularly careful during vacation

season because identity thieves come out in droves. That

makes it pivotal that consumers keep their debit cards on ice,

said Beth Givens, director of the Privacy Rights Clearing House

and one of the nation's foremost experts on keeping your

private information private.

What makes debit cards so dangerous? Givens has so many

reasons, her organization has put out an exhaustive fact sheet

on whether you should use cash, credit or debit cards when

shopping. (The report also explains the shortcomings of gift

cards.)

Here's the short version

of the dangers of debit:

1. Loss Limits ----knowledgefinancial.

com

Like credit cards, federal law limits your liability for fraudulent

transactions on a debit card to $50. But that's only if you notify

your financial institution within two days of discovering the

theft. If you're a space cadet and don't check your bank

statements for a couple of months, you could lose everything

2. Pay Now/Reimburse Later

If someone has fraudulently used your credit card, you don't

have to pay the charge. But when somebody has fraudulently

used your debit card, the money comes directly out of your

account in real time.

That means you're out the money while the bank does a

leisurely examination of their records to investigate your fraud

claim. Many consumers complaining to Privacy Rights Clearing

House said they lost access to their funds for several weeks.

In the meantime, they were caught short and unable to pay

their bills, Givens said.

3. Merchant Disputes ---

KNOWLEDGEFINANCIAL.COM

The same problem affects merchant disputes. If you pay with a

credit card when ordering something online, and that product

comes damaged, broken or not at all, you can dispute the

charge and stop payment with your credit card. If you used

your debit card, the charge is paid when you made the order.

By the time you find out the goods weren't what was

advertised, the merchant has your cash and you're in the

unenviable position of having to fight to get your money back.

4. Phantom Charges ----

KNOWLEDGEFINANCIAL.COM

If you use a credit card at a hotel, the hotel takes an imprint

when you check in, but doesn't charge your card until you

check out. It's a far different story with a debit card. Generally,

hotels will put a “hold” on funds in your account for more than

you're spending. Yes, more.

They hold the full amount of your stay, plus an estimated

amount for “incidentals,” such as meals at the hotel

restaurant and dipping into the mini-bar. This is not an actual

charge–the hold will come off your account at the end of your

stay.

But it affects the available balance in your checking account

anyway and can lead to overdrafts. One consumer said these

phantom charges cost him $140 in overdraft fees. These

“holds” are commonly placed on debit card transactions made

at hotels, gas stations and rental car companies.

5. Overdrafts, Overdrafts and

More Overdrafts ---

Overdraft charges have been soaring in recent years and the

vast majority of consumers who pay them explain that their

overdraft was the result of a debit card transaction. Many

consumers naively assumed that if they didn't have sufficient

funds in their accounts, their bank wouldn't approve a debit

swipe.

But they were wrong. The

result: a $4 coffee could

trigger a $35 overdraft fee.

Government regulators are reigning in these fees by

demanding that banks give consumers a chance to “opt out”

of automatic overdraft protection, but that doesn't start for

existing accounts until August. (If you have a new account, it's

starts in July.)

6. Skimming ----KNOWLEDGEFINANCIAL.COM

Financial crooks have gotten sophisticated in recent years and

are using “skimming” machines to read your card data and

charge your account, Givens said. When your debit card is

skimmed, your bank account can be drained before you know

that you've been had. ----KNOWLEDGEFINANCIAL.COM

THE DANGER OF DEBIT/CREDIT

CARDS!

The Dangers of Using a

Debit Card. ---knowledgefinancial.com ----

PLACES AND WAYS NOT

RECOMMENDED TO USE

DEBIT CARDS:

Consumers need to be particularly careful during vacation

season because identity thieves come out in droves. That

makes it pivotal that consumers keep their debit cards on ice,

said Beth Givens, director of the Privacy Rights Clearing House

and one of the nation's foremost experts on keeping your

private information private.

What makes debit cards so dangerous? Givens has so many

reasons, her organization has put out an exhaustive fact sheet

on whether you should use cash, credit or debit cards when

shopping. (The report also explains the shortcomings of gift

cards.)

Here's the short version

of the dangers of debit:

1. Loss Limits ----knowledgefinancial.

com

Like credit cards, federal law limits your liability for fraudulent

transactions on a debit card to $50. But that's only if you notify

your financial institution within two days of discovering the

theft. If you're a space cadet and don't check your bank

statements for a couple of months, you could lose everything

2. Pay Now/Reimburse Later

If someone has fraudulently used your credit card, you don't

have to pay the charge. But when somebody has fraudulently

used your debit card, the money comes directly out of your

account in real time.

That means you're out the money while the bank does a

leisurely examination of their records to investigate your fraud

claim. Many consumers complaining to Privacy Rights Clearing

House said they lost access to their funds for several weeks.

In the meantime, they were caught short and unable to pay

their bills, Givens said.

3. Merchant Disputes ---

KNOWLEDGEFINANCIAL.COM

The same problem affects merchant disputes. If you pay with a

credit card when ordering something online, and that product

comes damaged, broken or not at all, you can dispute the

charge and stop payment with your credit card. If you used

your debit card, the charge is paid when you made the order.

By the time you find out the goods weren't what was

advertised, the merchant has your cash and you're in the

unenviable position of having to fight to get your money back.

4. Phantom Charges ----

KNOWLEDGEFINANCIAL.COM

If you use a credit card at a hotel, the hotel takes an imprint

when you check in, but doesn't charge your card until you

check out. It's a far different story with a debit card. Generally,

hotels will put a “hold” on funds in your account for more than

you're spending. Yes, more.

They hold the full amount of your stay, plus an estimated

amount for “incidentals,” such as meals at the hotel

restaurant and dipping into the mini-bar. This is not an actual

charge–the hold will come off your account at the end of your

stay.

But it affects the available balance in your checking account

anyway and can lead to overdrafts. One consumer said these

phantom charges cost him $140 in overdraft fees. These

“holds” are commonly placed on debit card transactions made

at hotels, gas stations and rental car companies.

5. Overdrafts, Overdrafts and

More Overdrafts ---

Overdraft charges have been soaring in recent years and the

vast majority of consumers who pay them explain that their

overdraft was the result of a debit card transaction. Many

consumers naively assumed that if they didn't have sufficient

funds in their accounts, their bank wouldn't approve a debit

swipe.

But they were wrong. The

result: a $4 coffee could

trigger a $35 overdraft fee.

Government regulators are reigning in these fees by

demanding that banks give consumers a chance to “opt out”

of automatic overdraft protection, but that doesn't start for

existing accounts until August. (If you have a new account, it's

starts in July.)

6. Skimming ----KNOWLEDGEFINANCIAL.COM

Financial crooks have gotten sophisticated in recent years and

are using “skimming” machines to read your card data and

charge your account, Givens said. When your debit card is

skimmed, your bank account can be drained before you know

that you've been had. ----KNOWLEDGEFINANCIAL.COM

| Real Estate Is My Passion, That's What I Know Best. Any Help You Need, Any Questions You May Have About Real Estate In Florida. -- Feel Free To Contact Anthony |

Outrageous New-Car Scams To Avoid --

At the dealership people could well face a rude awakening at the

hands of a shady, even unscrupulous salesperson or new or used

-car dealership.

The dealership people love taking advantage because People are

not skilled at negotiating , while dealership personnel do it all day

every day. The field is not level from the start.”

According to the Better Business Bureau, issues with new-car

dealers remain among the top consumer complaints

Misrepresentations seem to be the most common complaints

among car buying consumers. We’ve documented 10 of the most

common new-car buying swindles, compiled with assistance

from the experts

At the dealership people could well face a rude awakening at the

hands of a shady, even unscrupulous salesperson or new or used

-car dealership.

The dealership people love taking advantage because People are

not skilled at negotiating , while dealership personnel do it all day

every day. The field is not level from the start.”

According to the Better Business Bureau, issues with new-car

dealers remain among the top consumer complaints

Misrepresentations seem to be the most common complaints

among car buying consumers. We’ve documented 10 of the most

common new-car buying swindles, compiled with assistance

from the experts

. "Back End" Add-Ons

Outrageous New-Car Scams To Avoid

There are far more ways for a dealership to make

money and there’s no more profitable way that the so-

called “back end” of the deal. In addition to financing,

you’ll be offered – perhaps pressured is a better word

– to purchase assorted add-ons that can suck the

value out of what would otherwise be a good deal.

These range from credit life insurance (conventional

term-life or disability insurance is usually a better buy)

to fabric protection (a can of Scotchguard can

suffice), rustproofing (largely unnecessary with today’

s cars) and paint sealant (little more than a good coat

of wax).

Simply refuse to pay for any of these high-profit items

and threaten to walk out on the deal if they’re insisted

upon.

Buying a costly service contract that extends a

manufacturer’s warranty for an additional two years or

more may seem like a good idea, but they’re just

insurance policies in which the actuarial odds favor

the house and rarely deliver any real value for the

money. If you feel it’s a necessity,

try to get the dealer to lower the price or, better yet,

shop around after the fact (or even ahead of time) to

find one for less money.

Outrageous New-Car Scams To Avoid

There are far more ways for a dealership to make

money and there’s no more profitable way that the so-

called “back end” of the deal. In addition to financing,

you’ll be offered – perhaps pressured is a better word

– to purchase assorted add-ons that can suck the

value out of what would otherwise be a good deal.

These range from credit life insurance (conventional

term-life or disability insurance is usually a better buy)

to fabric protection (a can of Scotchguard can

suffice), rustproofing (largely unnecessary with today’

s cars) and paint sealant (little more than a good coat

of wax).

Simply refuse to pay for any of these high-profit items

and threaten to walk out on the deal if they’re insisted

upon.

Buying a costly service contract that extends a

manufacturer’s warranty for an additional two years or

more may seem like a good idea, but they’re just

insurance policies in which the actuarial odds favor

the house and rarely deliver any real value for the

money. If you feel it’s a necessity,

try to get the dealer to lower the price or, better yet,

shop around after the fact (or even ahead of time) to

find one for less money.

- Outrageous New-Car Scams To Avoid -

The Spot Delivery Scam

Perhaps among the most onerous of car-deal cons,

this swindle involves sending a buyer – often one

with sub-prime credit – home in a new vehicle before

the final financing arrangements have been

completed.

The dealer calls back in a day or two to tell the

customer there’s a problem with the loan terms,

subsequently subjecting him or her to a higher

interest rate than expected and perhaps even

requiring a larger down payment in order to qualify.

The idea is that since the buyer has emotionally

“bonded” with the vehicle by already taking

possession, he or she will pay whatever it takes to

keep it.

Again, the best defense here is to shop around ahead

of time for financing, especially to be aware of for

which rates and terms you’ll qualify given your credit

rating.

---------------------------------

Negative Equity Scams

Never trust dealers who promise to pay off your

existing car loan – no matter how much you owe on it.

Motorists who’ve bought their current vehicles with

low down payments and long loan terms often have

“negative equity” in them, meaning they owe more

than the car is worth in trade.

Sure, the dealer will pay off the loan, but will simply

wrap the amount of negative equity into the new-car

deal, resulting in a higher balance, a costlier monthly

payment and even a longer loan term.

You’ll also be in the uncomfortable position of paying

for two cars at the same time. It’s better to hold onto

your current car until it’s paid for, or at least until the

balance is whittled down sufficiently to realize actual

equity.

The Spot Delivery Scam

Perhaps among the most onerous of car-deal cons,

this swindle involves sending a buyer – often one

with sub-prime credit – home in a new vehicle before

the final financing arrangements have been

completed.

The dealer calls back in a day or two to tell the

customer there’s a problem with the loan terms,

subsequently subjecting him or her to a higher

interest rate than expected and perhaps even

requiring a larger down payment in order to qualify.

The idea is that since the buyer has emotionally

“bonded” with the vehicle by already taking

possession, he or she will pay whatever it takes to

keep it.

Again, the best defense here is to shop around ahead

of time for financing, especially to be aware of for

which rates and terms you’ll qualify given your credit

rating.

---------------------------------

Negative Equity Scams

Never trust dealers who promise to pay off your

existing car loan – no matter how much you owe on it.

Motorists who’ve bought their current vehicles with

low down payments and long loan terms often have

“negative equity” in them, meaning they owe more

than the car is worth in trade.

Sure, the dealer will pay off the loan, but will simply

wrap the amount of negative equity into the new-car

deal, resulting in a higher balance, a costlier monthly

payment and even a longer loan term.

You’ll also be in the uncomfortable position of paying

for two cars at the same time. It’s better to hold onto

your current car until it’s paid for, or at least until the

balance is whittled down sufficiently to realize actual

equity.

Outrageous New-Car Scams To Avoid

Finessed Financing

Automakers regularly offer cut-rate financing on select

models through their affiliated finance companies that

can be real money savers. Unfortunately, as the ads

state they’re reserved “for qualified buyers only.”

While lenders have been easing up on their credit

qualifications in recent months, only those with top

FICO scores (usually 690 or better out of a maximum

850) will even come close to qualifying for the most

favorable financing terms.

Everyone else will be asked to pay higher rates and

sometimes even a higher down payment; if your credit

is particularly tarnished, you’ll pay dearly. Even those

with stellar credit might find themselves being quoted

a higher rate at the dealership than they might garner

elsewhere.

Facilitating financing is a major profit center for new-

car dealers. Always shop around for a car loan ahead

of time among local banks (and a credit union if you’re

a member) to find the lowest rates for which you

qualify. If the dealer can do better thanks to a

promotional financing plan, so much the better; if not

obtain a lower-cost loan elsewhere.

Finessed Financing

Automakers regularly offer cut-rate financing on select

models through their affiliated finance companies that

can be real money savers. Unfortunately, as the ads

state they’re reserved “for qualified buyers only.”

While lenders have been easing up on their credit

qualifications in recent months, only those with top

FICO scores (usually 690 or better out of a maximum

850) will even come close to qualifying for the most

favorable financing terms.

Everyone else will be asked to pay higher rates and

sometimes even a higher down payment; if your credit

is particularly tarnished, you’ll pay dearly. Even those

with stellar credit might find themselves being quoted

a higher rate at the dealership than they might garner

elsewhere.

Facilitating financing is a major profit center for new-

car dealers. Always shop around for a car loan ahead

of time among local banks (and a credit union if you’re

a member) to find the lowest rates for which you

qualify. If the dealer can do better thanks to a

promotional financing plan, so much the better; if not

obtain a lower-cost loan elsewhere.

Outrageous New-Car Scams To

Avoid

Fun With Numbers

There’s a lot of paperwork involved in buying a new

vehicle, and wading through it all can become

unnerving when a salesperson or finance manager is

waiting impatiently for you to sign at the bottom of

each page.

Those with an aversion to numbers and/or lacking

math skills can find themselves at a distinct

disadvantage. “Mistakes” in paperwork are common,

and to no one’s surprise they usually favor the dealer.

The price of the car or trade-in value may not exactly

be what’s been agreed upon or the interest rate

quoted may be inflated. Sometimes the discrepancies

can be flagrant, such as when a buyer is asked to sign

a leasing agreement thinking it was actually a sales

contract, or when the value of a trade-in is

“inadvertently” left out. In other cases the numbers

may simply be off by a few hundred dollars or a half

percent.

Always take the time to read all documents carefully,

make sure the numbers all jibe with what’s been

agreed upon and use a calculator to check the math

before signing anything. And refuse to pay for

spurious charges that may suddenly appear in the

paperwork, like for “prep” and “advertising” that are

essentially part of the dealer’s cost of doing business.

---------------------------------------

Trade-In Tribulations

While a new-car buyer can usually get the most for his

or her current ride by selling it outright to a private

party, this is a time consuming process that’s fraught

with its own elements of peril. That’s why most

consumers choose the convenience of trading-in their

cars at a dealership and using the proceeds as part (or

all) of the down payment on a new model.

Unfortunately a dealer may artificially inflate the value

of your trade-in to help seal a deal and ultimately exact

that cost – often more – by manipulating other aspects

of the transaction. Always research the estimated

trade-in value of a car ahead of time via an car

valuation web site like Kelley Blue Book or NADA

Guides to get an idea of what it might be worth,

and always negotiate the trade-in value separately

from the new car’s price. It’s often worthwhile to bring

a car in to the dealership’s used car department and

get a bona fide trade-in quote ahead of time.

Beware that salespeople have been known to hold the

keys to a trade-in “hostage” while negotiating to

pressure customers to buy a new car, so never just

hand them over – always accompany the salesperson

or used-car manager while they’re giving your trade-in

a once-over.

Avoid

Fun With Numbers

There’s a lot of paperwork involved in buying a new

vehicle, and wading through it all can become

unnerving when a salesperson or finance manager is

waiting impatiently for you to sign at the bottom of

each page.

Those with an aversion to numbers and/or lacking

math skills can find themselves at a distinct

disadvantage. “Mistakes” in paperwork are common,

and to no one’s surprise they usually favor the dealer.

The price of the car or trade-in value may not exactly

be what’s been agreed upon or the interest rate

quoted may be inflated. Sometimes the discrepancies

can be flagrant, such as when a buyer is asked to sign

a leasing agreement thinking it was actually a sales

contract, or when the value of a trade-in is

“inadvertently” left out. In other cases the numbers

may simply be off by a few hundred dollars or a half

percent.

Always take the time to read all documents carefully,

make sure the numbers all jibe with what’s been

agreed upon and use a calculator to check the math

before signing anything. And refuse to pay for

spurious charges that may suddenly appear in the

paperwork, like for “prep” and “advertising” that are

essentially part of the dealer’s cost of doing business.